seajay wrote: ↑Sat Oct 23, 2021 1:15 pm

murphy_p_t wrote: ↑Sat Oct 23, 2021 12:53 pm

seajay wrote: ↑Sat Oct 23, 2021 8:06 am

For the method I outlined earlier and from 1900 ...

4% was more a PWR, and in one case you ended with over seven times the inflation adjusted start date portfolio value after 4% SWR withdrawals (a additional 6,7% annualized real on top).

BUT that did direct towards around a 75/25 stock/Precious Metal broad average (since 1933).

Fundamentally stocks are leveraged, of the order $30T cap versus $9T for corporate bond cap. Leverage broadly just scales volatility, not rewards, so its reasonable to deleverage i.e. allocate $30 to stocks, $9 to corporate bonds, which with rounding is close to 75/25 stock/bond proportions. Corporate bonds pay higher premiums reflective of their default rate,

so 10 year Treasury might be substituted in instead. Or even

gold (or silver).

Mix in some averaging such as two timepoint entry to avoid loading fully in at the worst possible start date, and some relative valuation ... and overall rewards at least historically were satisfactory (good chance of your money outliving you).

Silver was used in the above on the grounds of the US outlawing investment gold between 1940's and 1970's. Outside of that and where investment gold was permitted it worked to similar effect.

To reiterate that is based on the assumption that pre 1933 when on the gold standard investors might have preferred to hold just bonds (T-Bills/whatever), but where during WW1 years the investor might have rotated into silver. From 1933 the relative Dow/Gold ratio directed the amount of PM to start each year with (relative valuation).

Seajay... Very interesting concept. I was recently thinking of deviating from the pp in a direction like this.

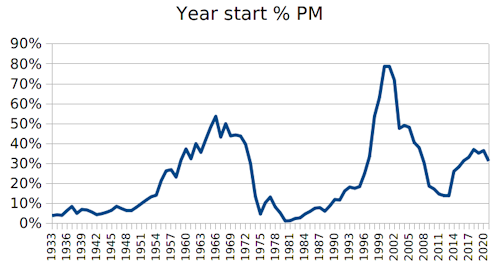

Can you include a chart showing percent PM versus year?

Also, what are the units in your first chart?

Units in the first chart are multiples of original inflation adjusted start date amount remaining after 30 years, so 1 = 100% of the inflation adjusted original amount, 2 = twice as much ...etc.

Year start % PM ...

Dow/Gold ratio data (year start values)

Code: Select all

1933 2.9

1934 3.1

1935 3.0

1936 4.1

1937 5.1

1938 3.5

1939 4.4

1940 4.3

1941 3.8

1942 3.1

1943 3.4

1944 3.7

1945 4.2

1946 5.2

1947 4.6

1948 4.2

1949 4.2

1950 4.9

1951 5.8

1952 6.7

1953 7.5

1954 7.9

1955 11.5

1956 13.9

1957 14.2

1958 12.4

1959 16.6

1960 19.3

1961 16.9

1962 20.6

1963 18.4

1964 21.6

1965 24.7

1966 27.3

1967 22.2

1968 25.5

1969 22.5

1970 22.7

1971 22.4

1972 20.5

1973 15.8

1974 7.6

1975 3.3

1976 6.1

1977 7.5

1978 5.0

1979 3.6

1980 1.6

1981 1.6

1982 2.2

1983 2.3

1984 3.3

1985 3.9

1986 4.7

1987 4.9

1988 4.0

1989 5.3

1990 6.9

1991 6.7

1992 9.0

1993 9.9

1994 9.6

1995 10.0

1996 13.2

1997 17.4

1998 27.3

1999 31.9

2000 39.5

2001 39.6

2002 36.2

2003 24.3

2004 25.1

2005 24.6

2006 20.9

2007 19.6

2008 15.9

2009 10.1

2010 9.4

2011 8.2

2012 7.8

2013 7.9

2014 13.8

2015 14.9

2016 16.4

2017 17.2

2018 19.1

2019 18.3

2020 18.9

2021 16.3

Year start Dow/Gold ratio

Stochastic of 1 lower, 50 upper

( current - lower ) / ( upper - lower )

So yearly value - 1 divided by 49

i.e. year start 2021 Dow/Gold ratio 16.3 so 15.3 / 49 = 0.31 (31% PM, so 69% stock).

Given a indicator of %PM, then on the stock side let Buffett take care of appropriate %cash reserves ...

Code: Select all

Inflation BRK Gold Dow/Gold %PM Portfolio

1986 1.10% 14.17% 18.96% 4.7 7.6% 14.5%

1987 4.43% 4.61% 24.53% 4.9 8.0% 6.2%

1988 4.42% 59.32% -15.26% 4 6.1% 54.8%

1989 4.65% 84.57% -2.84% 5.3 8.8% 76.9%

1990 6.11% -23.05% -3.11% 6.9 12.0% -20.6%

1991 3.06% 35.58% -8.56% 6.7 11.6% 30.4%

1992 2.90% 29.83% -5.73% 9 16.3% 24.0%

1993 2.75% 38.94% 17.68% 9.9 18.2% 35.1%

1994 2.67% 24.96% -2.17% 9.6 17.6% 20.2%

1995 2.54% 57.35% 0.98% 10.1 8.4% 47.0%

1996 3.32% 6.23% -4.59% 13.2 24.9% 3.5%

1997 1.70% 34.90% -21.41% 17.4 33.5% 16.1%

1998 1.61% 52.17% -0.83% 27.3 53.7% 23.7%

1999 2.68% -19.86% 0.85% 31.9 63.1% -6.8%

2000 3.39% 26.56% -5.44% 39.5 78.6% 1.4%

2001 1.55% 6.48% 0.75% 39.6 78.8% 2.0%

2002 2.38% -3.77% 25.57% 36.2 71.8% 17.3%

2003 1.88% 15.81% 19.89% 24.3 47.6% 17.8%

2004 3.26% 4.33% 4.65% 25.1 49.2% 4.5%

2005 3.42% 0.82% 17.77% 24.6 48.2% 9.0%

2006 2.54% 24.11% 23.20% 20.9 40.6% 23.7%

2007 4.08% 28.74% 31.92% 19.6 38.0% 29.9%

2008 0.09% -31.78% 4.32% 15.9 30.4% -20.8%

2009 2.72% 2.69% 25.04% 10.1 18.6% 6.8%

2010 1.50% 21.42% 29.24% 9.4 17.1% 22.8%

2011 2.96% -4.73% 8.93% 8.2 14.7% -2.7%

2012 1.74% 16.82% 8.26% 7.8 13.9% 15.6%

2013 1.50% 32.70% -27.33% 7.9 14.1% 24.2%

2014 0.76% 27.04% 0.12% 13.8 26.1% 20.0%

2015 0.73% -12.48% -12.11% 14.9 28.4% -12.4%

2016 2.07% 23.42% 8.10% 16.4 31.4% 18.6%

2017 2.11% 21.91% 12.66% 17.2 33.1% 18.9%

2018 1.91% 2.82% -0.93% 19.1 36.9% 1.4%

2019 2.29% 10.98% 18.43% 18.3 35.3% 13.6%

2020 1.36% 2.42% 24.61% 18.9 36.5% 10.5%

16.3 31.2%

A couple of quick questions:

1. In your 1900-present return chart did you use silver for 1914-1918 (or perhaps 1914-1919) or did you use T-Bills? If you used silver during the inflationary WWI years but then

DIDN'T use it during the deflationary mid-year 1920 through late 1920s period then this is kind of "loading the dice" a bit and overstating portfolio returns for the whole period 1914-1929.

2. Did you use silver for 1933 or gold?

3. Did you stop using silver in 1971, 1972, 1973, 1974, or at the beginning of 1975? In other words, what year did you start using gold in the portfolio in lieu of silver? Or did you just always use silver from 1933 onward until today and never use gold?

4. While I personally have Berkshire annual returns back to 1964 and Buffett Partnership (LP) returns back to 1957 for before that if needed for backtesting something like this I do have to ask....don't you think it is a bit of a survivorship bias stretch to use only Berkshire as the "stock" portion of the holdings? One, not everyone knew about Warren Buffett and Berkshire Hathaway; he wasn't nearly as famous as he is now until (arguably) the mid-1980s; two, Buffet's returns from, say, 1957 to 1995 or so are unlikely to be repeated for several reasons (first, in the very early years of Buffet's investing career--say the late 50s to the mid-1970s--stocks were a lot cheaper and lower PE than they are now; second, from the mid-60s to the mid-90s Berkshire itself was a good bit smaller than today and thus could deploy its capital more nimbly into potentially higher returning smaller and midcap issues rather than only being able to focus on large caps like today's Berkshire is forced to do when it wants to acquire a company; and third, eventually Buffett--and for that matter Munger--will be dead and thus Berkshire won't have their investment expertise any more); three, using only Berkshire doesn't include the many insurance or reinsurance or holding companies that weren't nearly as successful as Berkshire Hathaway was (i.e. classic survivorship bias). FWIW I do think Berkshire will continue to beat the market over the long-run; using interest-free insurance premium float to buy good, stable, richly cash-flowing companies is an excellent business strategy.....I just don't think it will beat it by anywhere near the 8 or 9% annually on average that Buffett has beaten the market by since he started investing (indeed, as per Warren Buffett's own admission his returns over the last 20-25 years or so are nowhere near what he was able to achieve in Berkshire's earlier days).