I mentioned New Year's resolution #1 in the 2019 results thread (reduce portfolio checking). Here's another one: Simplify the holdings.

This past year, I consolidated a few accounts (HSA, online banking) to sub-accounts at Fidelity. Well worth it! But, I've now collected a bunch of different holdings. Now that commissions are no longer a thing, it's time to consolidate them to simplify the record-keeping and management. In short, I'm sick of holding too much stuff.

I realize though, that this desire for simplification goes against the standard advice on diversifying holdings. This would mean diversifying across institutions, investment vehicle types, and specific funds. So how much diversification do you really need? In addition to Fidelity, I have an account at Vanguard whose job it is to hold their Treasury money market fund as well as a stock fund. I also have accounts at Perth Mint and Treasury Direct, plus some physical gold. To me that is enough! Probably too much, actually.

There's also the perennial issue of funds vs individual securities. To some degree I've done the individual holding thing in all 4 asset classes, and I figure this gives me license to use just one fund (e.g. FNGBX for bonds) for the rest of my holdings within an asset/account.

Anyone else experiencing portfolio clutter??

Portfolio simplification vs. diversification

Moderator: Global Moderator

Re: Portfolio simplification vs. diversification

Good topic, Sophie! Very curious to hear others' thoughts.

This past year I have tried to consolidate accounts - most now lives at Schwab. Rolled over a previous employer's 401k, moved a rollover IRA, and transferred assets from another brokerage account. Also closed out bank accounts I held at other institutions and moved the money into one.

I just went through the process of sorting through all my paper statements for the year (making a big shred pile, as I'm still one of those folks who likes paper statements), and it's nice reducing the clutter to fewer accounts. However, I do worry a bit about consolidating to fewer points of institutional failure. I'm basically down to Schwab, Vanguard, TreasuryDirect, a local credit union for daily banking, and an internet bank.

The diligence to account/prepare for uncommon "what if" scenarios does have a cost. It's nice to minimize that, but hoping it doesn't come back to bite me. I'm not sure where the right balance lies...

This past year I have tried to consolidate accounts - most now lives at Schwab. Rolled over a previous employer's 401k, moved a rollover IRA, and transferred assets from another brokerage account. Also closed out bank accounts I held at other institutions and moved the money into one.

I just went through the process of sorting through all my paper statements for the year (making a big shred pile, as I'm still one of those folks who likes paper statements), and it's nice reducing the clutter to fewer accounts. However, I do worry a bit about consolidating to fewer points of institutional failure. I'm basically down to Schwab, Vanguard, TreasuryDirect, a local credit union for daily banking, and an internet bank.

The diligence to account/prepare for uncommon "what if" scenarios does have a cost. It's nice to minimize that, but hoping it doesn't come back to bite me. I'm not sure where the right balance lies...

Re: Portfolio simplification vs. diversification

Sophie! Yes!

That’s a funny coincidence. Right in my sig I’ve conceded that I’ve simplified my portfolio with a two fund implementation of the PP.

I started a thread about this way back, and I essentially revisited the idea and decided that I liked it.

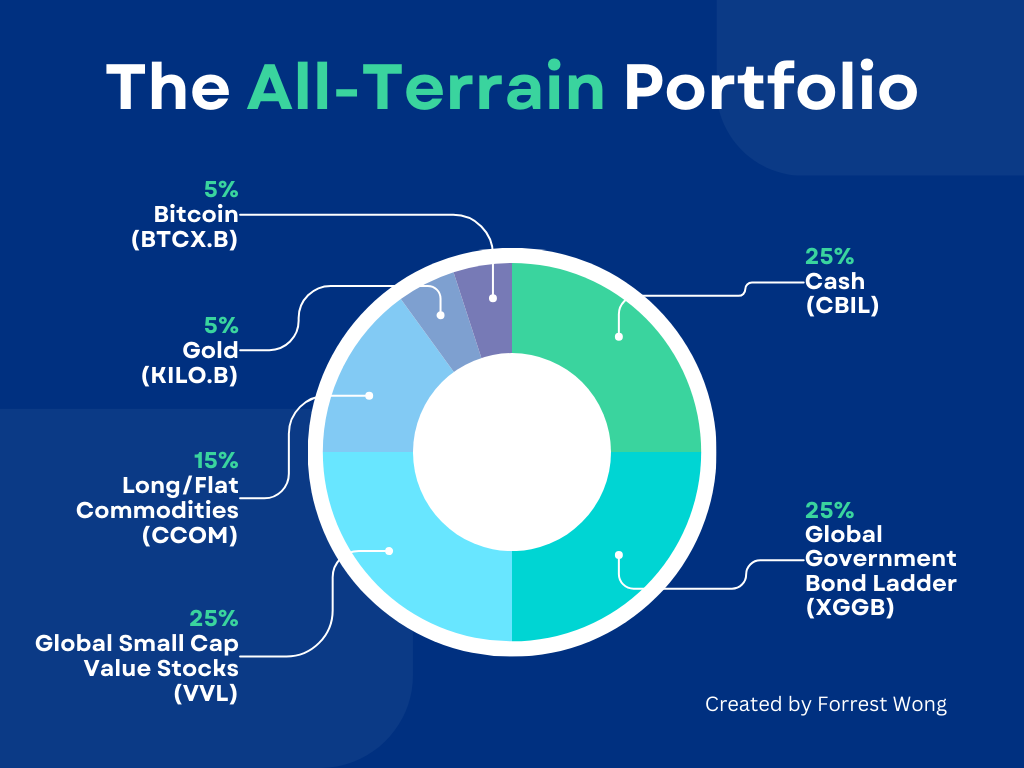

75% of my money is in a vanguard conservative fund. This covers stocks, bonds, and cash. The other 25% is in the lowest cost gold ETF in Canada which is KILO.B.

I also have some physical gold coins and my daily spending cash at the bank. Super simple!

viewtopic.php?f=1&t=9613

Above is a link to the thread I started.

That’s a funny coincidence. Right in my sig I’ve conceded that I’ve simplified my portfolio with a two fund implementation of the PP.

I started a thread about this way back, and I essentially revisited the idea and decided that I liked it.

75% of my money is in a vanguard conservative fund. This covers stocks, bonds, and cash. The other 25% is in the lowest cost gold ETF in Canada which is KILO.B.

I also have some physical gold coins and my daily spending cash at the bank. Super simple!

viewtopic.php?f=1&t=9613

Above is a link to the thread I started.

DITM

www.allterraininvesting.com

www.allterraininvesting.com

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Portfolio simplification vs. diversification

I use fidelity for 90% and chase for 10% ...it is important to have a local source for money and bill paying ..

Fidelity has their own hackers who scan the dark web for anything pertaining to fidelity ...they saw my wife’s info up there...not that they could do much with it ..fidelity notified us and closed those accounts down ..it took about 10 days to get all new checks , cards and accounts

Fidelity has their own hackers who scan the dark web for anything pertaining to fidelity ...they saw my wife’s info up there...not that they could do much with it ..fidelity notified us and closed those accounts down ..it took about 10 days to get all new checks , cards and accounts

Re: Portfolio simplification vs. diversification

Yup! It's something I have to actively counter.

As an engineer, I typically change jobs every few years, so I get new accounts for my 401k, HSA, and brokerage for RSUs. So I usually consolidate by transferring the accounts from my old job into my new accounts. Even if some of the institutions are the same, the account numbers are different, so consolidation is still necessary to avoid portfolio clutter.

Reducing the clutter is a bit of a pain, but at least I only have to do it every few years. I think it's worthwhile.

Re: Portfolio simplification vs. diversification

Thanks for the link! I didn't remember that thread at all, but it looks like the discussion was mostly about whether to go international and also about the silver, so I probably didn't catch the simplicity part of it.Smith1776 wrote: ↑Wed Jan 01, 2020 1:52 pm 75% of my money is in a vanguard conservative fund. This covers stocks, bonds, and cash. The other 25% is in the lowest cost gold ETF in Canada which is KILO.B.

I also have some physical gold coins and my daily spending cash at the bank. Super simple!

viewtopic.php?f=1&t=9613

Above is a link to the thread I started.

I would hesitate to do this for myself though. As Einstein once said, "Everything should be made as simple as possible, but not simpler." One of the best mechanisms in the PP is the bond/cash barbell. It's been discussed here ad nauseum, but the major benefits are: 1) it allows you to integrate your emergency fund into the portfolio rather than holding it separately, 2) the rebalancing mechanism gives you an automatic program for keeping your cash reserves topped up, and 3) the presence of the cash allocation allows you to avoid having to sell volatile assets when they're down. Also, keeping the assets separate makes it much easier to manage the tax consequences of drawing money from the portfolio. With the balanced fund, you have to sell all 3 assets at the same time when you need to draw from it. This is probably OK for a 401K account during your accumulation years though.

I'm happy that people like the portfolio decluttering concept though! I genuinely don't know how much diversification is "enough", so looking forward to the discussion. Carry on!

Re: Portfolio simplification vs. diversification

I have been trying to simplify portfolio clutter while simultaneously tweaking overall tax efficiency:

1. I closed two relatively smallish accounts, a SEP IRA and my wife’s traditional IRA, by converting and consolidating them both into our Roth IRAs. I did this at the same I did my annual Roth IRA conversion. It took a while to do this over the phone with a Fidelity rep, but I think it will be worthwhile in the long run.

2. The recent discussions surrounding the changes in “stretch” IRAs due to passage of the SECURE Act prompted me to consider re-structuring an inherited IRA. I originally filled this account with classic 4 x 25 HBPP ETFs, but the prospect of mandatory future Required Minimum Distributions from this account starting in 2019 made me re-think asset placement. I now intend to fill the inherited IRA with just FDLXX, which will free up more space for the three volatile assets in my Roth IRA. That in turn will hopefully result in more compounded tax-free growth over time.

I agree that you have to strike a balance between simplicity and diversification. The barbell of Cash and Bonds is a perfect example of this balance. You can theoretically have the same yield with just Intermediate T-bonds, but it is simply not as flexible as holding both assets.

1. I closed two relatively smallish accounts, a SEP IRA and my wife’s traditional IRA, by converting and consolidating them both into our Roth IRAs. I did this at the same I did my annual Roth IRA conversion. It took a while to do this over the phone with a Fidelity rep, but I think it will be worthwhile in the long run.

2. The recent discussions surrounding the changes in “stretch” IRAs due to passage of the SECURE Act prompted me to consider re-structuring an inherited IRA. I originally filled this account with classic 4 x 25 HBPP ETFs, but the prospect of mandatory future Required Minimum Distributions from this account starting in 2019 made me re-think asset placement. I now intend to fill the inherited IRA with just FDLXX, which will free up more space for the three volatile assets in my Roth IRA. That in turn will hopefully result in more compounded tax-free growth over time.

I agree that you have to strike a balance between simplicity and diversification. The barbell of Cash and Bonds is a perfect example of this balance. You can theoretically have the same yield with just Intermediate T-bonds, but it is simply not as flexible as holding both assets.

“Groucho Marx wrote:

A stock trader asked him, "Groucho, where do you put all your money?" Groucho was said to have replied, "In Treasury bonds", and the trader said, "You can't make much money on those." Groucho said, "You can if you have enough of them!"

A stock trader asked him, "Groucho, where do you put all your money?" Groucho was said to have replied, "In Treasury bonds", and the trader said, "You can't make much money on those." Groucho said, "You can if you have enough of them!"

-

dualstow

- Executive Member

- Posts: 14292

- Joined: Wed Oct 27, 2010 10:18 am

- Location: synagogue of Satan

- Contact:

Re: Portfolio simplification vs. diversification

No clutter with regard to having too many accounts.

As for holdings, I used to agonize about getting rid small-cap and mid-cap stock blend funds without a tax bite. Nowadays, I don't agonize so much as deliberate.

Do indy stocks constitute clutter? I try to think of my Vp as a homemade Wellesley.

As for holdings, I used to agonize about getting rid small-cap and mid-cap stock blend funds without a tax bite. Nowadays, I don't agonize so much as deliberate.

Do indy stocks constitute clutter? I try to think of my Vp as a homemade Wellesley.

9pm EST Explosions in Iran (Isfahan) and Syria and Iraq. Not yet confirmed.