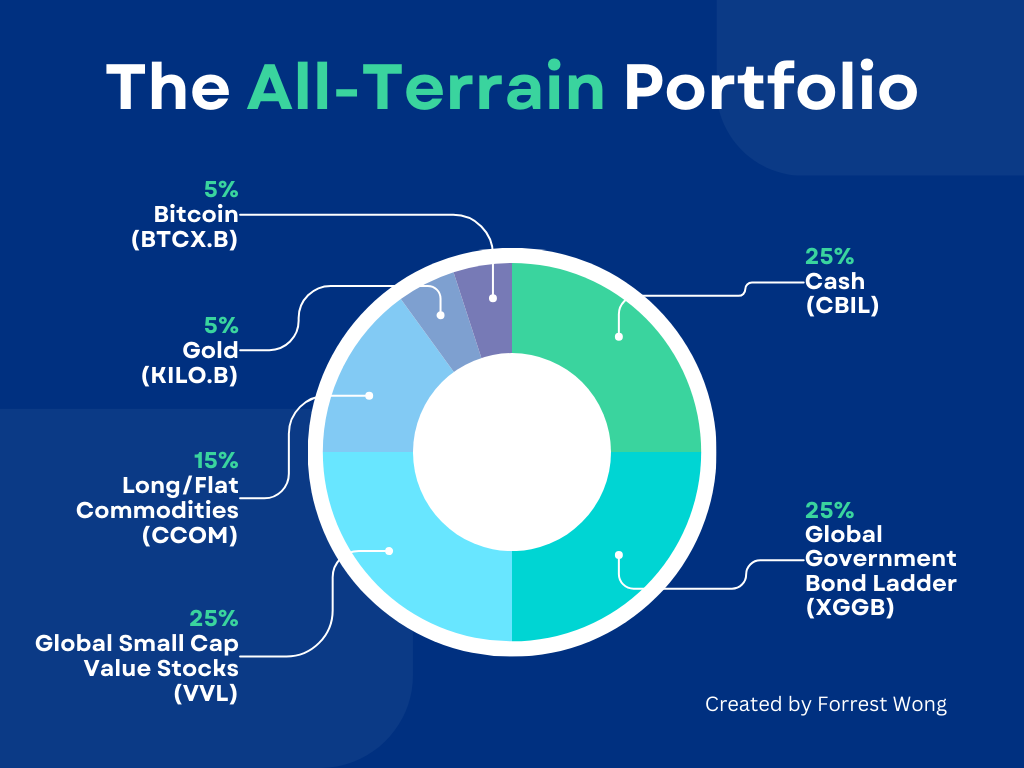

My asset allocation prior to learning of and investing in the HBPP was:

30% Total Stock Market Index Fund

20% Total International Stock Market Index Fund

5% REIT Fund

10% Long Term Treasury Bond Mutual Fund

5% Gold/Silver

20% Variable Portfolio of individual stocks that I actively traded

10% Cash

I wasn't too far off the HBPP path. I knew gold was important as a hedge against inflation. I knew long-term treasury bonds were a hedge against "bad stock market performance". I knew what deflation meant but not what it meant for my portfolio nor that long-term treasuries were good for it. I just knew that stocks and bonds moved in opposite directions and long-term treasuries moved the most dynamically, so I could have a greater exposure to stocks with less risk if I have more "aggressive" bonds. I knew costs mattered and tax efficiency mattered.

What I did not know, and soon learned was:

There's a marketing aspect involved in investments. I really wanted to invest in hedge funds because they had an exciting allure to them, and because I was told I couldn't, due to not having enough assets. I really wanted to invest in DFA funds because I was told I couldn't, and I even considered paying an investment advisor a hefty fee to be able to access DFA funds. I really wanted to invest in closed actively traded funds like Primecap and one of the Bridgeway Microcap funds, because I was told I couldn't. I really wanted to invest in Wellesley because they were around forever, had a great track record, and have a cool name. Wellesley Income Fund. Who wouldn't want to put money in there and see that cool name on their statements each month? I learned that investment/speculation options were like any other consumer product with regard to marketing psychology and I was falling prey to that.

There's 4 possible economic scenarios: recession, prosperity, inflation, deflation. Your portfolio needs to handle all of them.

Economics can tell us with certainty that something WILL happen (such as inflation when government prints more money), but economics cannot tell us WHEN it will happen.

Actively trading individual stocks, even if you do "research" such as reading 10Ks, is the equivalent of an amateur playing poker at against a table full of people who have won the World Series of Poker. You can get lucky on occasion, but you have no chance in the long term. You have no idea who is on the other end of each stock transaction you make, and very likely, they are professional traders who do this for a living full-time and have more information than you have.

There's an opportunity cost involved with thinking about your portfolio that takes away energy from the rest of your life.

Standard deviation and total portfolio volatility is important and while a young person can afford to take huge losses due to a long-enough investing timeline, it's suboptimal to have such volatility.

Domestic US stocks do significant business overseas and 25% of portfolio allocated to gold is sufficient in itself to hedge against US collapse or hyperinflation. If the US economy did collapse, in 2015, the rest of the world is coming with it, so there's no safety in international stocks.

There's no magic asset allocation. 4x25 is nothing magical and is definitely not the optimal ratio for the HBPP. However, no one can know what the optimal ratio is. If you knew bonds were going to be the best asset for a specific year, you'd be 100% in bonds. But you don't know that and you can't know that. You can back-test various permutations of the split such as 20-20-30-30 or 21-29-24-26, and figure out which variation of the ratios led to best results over the last 40 years, but you won't know which will lead to the best results for the next 40 years. If you let your portfolio work, every asset will be between 16% and 34% at any given time, so it won't actually be 4x25 anyway. Your portfolio is really not 4x25 and that's okay.

Harry Browne figured this whole HBPP out years ago so there's only four main types of discussions that can occur on an internet forum surrounding the HBPP:

1) Skeptics trying to understand the HBPP and supporters explaining it to interested parties

2) Haters who dislike the HBPP and will either poo poo the whole thing or argue for variations that are definitely not the HBPP

3) Long-time HBPP supporters and scholars who are looking to new market tools to enhance the PP while following the core tenets (such as ETFs that weren't available to HB: e.g. SGOL and IAU)

4) Non-HBPP discussion on topics that have a libertarian philosophy because (a) HB was a libertarian (b) people learning of the HBPP may have learned it because they knew of HB's libertarian politics (c) people who are smart enough to realize the HBPP is good are smart enough to also pick the only rational political ideology (d) people who people the HBPP have a selection bias in a distrust of government (leading them to 25% gold), and this aligns with libertarianism.

___________________

I'd estimate that I partially went into the PP about 5 years ago, just before the market crash, then gradually went deeper and deeper in, reducing my VP, until about 2 years ago when I went 100%. I no longer read threads or listen to HB radio episodes in order to "make sense" of it, or justify my reasoning for selecting it. HBPP just makes sense and barring some major global changes (such as the ability to cheaply make gold from lead), it will continue to make sense. Now, I spend significantly less life energy thinking about investments and the little time I do spend, I look for opportunities to "juice" the HBPP while sticking to the core tenets.

For example, using IBonds for some of the "cash" portion of the HBPP. The instruments should be as safe as t-bills but they have added inflation protection. In the event of a huge spike in short-term interest rates, tbills could easily lose 2% of their value. Whereas IBonds cannot, and may gain if the CPI numbers go up. In the event of deflation, IBonds can't go below face value, so this is an economic "free lunch". Of course, you can't put all of your cash into IBonds because (a) annual limits restricting investment levels and (b) they are less liquid because it would take at least a couple of weeks to sell the IBonds, ACH the money into a brokerage, let the ACH clear, and settle a stock/bond trade.

On the same topic of juicing returns, I read through multiple threads on using EE Bonds as the "Long Term Bond" portion, and in spite of good effort by the posters, it's not feasible and highly dangerous because you need marketable securities that can spike in face value. Having a good understanding of the HBPP allows me to read such threads critically and understand the speculative nature and variation from the core principles of the HBPP.

As far as the people who will poo poo the idea of juicing returns for a small marginal portfolio benefit, these are the same people who would jump at an opportunity for an ETF that charged a few basis points expense ratio lower than one they currently used. For example, if I only keep 20% of my cash in IBonds (which is 5% of my total portfolio), and if I can earn 1% greater return on those IBonds relative to TBills, then that's the equivalent of 0.05% portfolio gain, compounded annually, for free, forever. There's countless threads on Bogleheads about what 0.05% expenses will add up to over 40+ years. So, YES, it IS worth it to juice your HBPP when possible (assuming you don't deviate from the core principles).

This is most of what I've learned over the last six years.

Over the next six years I'd like to learn to not habitually check my portfolio. While I don't get stressed out at small drops, it does take mental focus and energy away from other life activities. I keep telling myself that the reason I check is to make sure hackers didn't wipe out my accounts and also because I'm on track for an "early retirement" and checking my progress on a regular basis helps keep me working towards that goal.

In one sense, early retirement for me is like a diet. You do things you don't want to do to become what you want to be. You avoid eating that cheeseburger because you want to lose weight and be in good shape. And if you check the scale every day (or twice a day), you are rewarded to see your weight is in check.

Similarly, you go to a job everyday that you may not like, and may have had a terrible day at work. Maybe you also avoid a purchase of something extravagant that you want, but don't need. And by checking your portfolio that night, and looking at your total net worth (up to date for all market conditions of that day), it helps to cope with the stress of the job (or budget) by seeing you're on track for the long-term goal.

Conversely, when on a diet, if you binge eat and look at the scale that day, you see you gained 2 pound and feel terrible. That keeps you from going off the diet the following day and back on track. And if you quit your job because your boss is an asshole, or splurged on a new $1,000 widget you didn't need, and check your total net worth to see it's dropped, then it gets you back on financial track to find a new job and go back on your budget.

That said, I'd like to achieve a life state where I do things that are conducive to long-term goals with the need for daily progress reports towards those goals (not checking the scale 2x a day and not checking my portfolio every night). That's my goal for the next 6 years