i use a dynamic method of spending in retirement .

4% of each years balance each dec 31st .

if markets are down i take 5% less then the previous draw or the same draw , which ever is higher .

if the 2nd year is down then it is the same story , 4% of the balance or 5% less , which ever is higher .

because it is dynamic it back tested out 1005 past 40 years of spending

Why the PP is better in accumulation than you think

Moderator: Global Moderator

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

You say you draw out 4% a year. Call me dumb but could you clarify how this works to keep you from depleting your core balance? You say if "the markets are down, you take less then 5% less of the previous draw." How much less? You are taking out on 4% so you would have a negative draw? Is that right? Can you explain this again in another way as I don't really have my head wrapped around it? example, you take 4% a year Dec 31st. The markets are down (how far down, the market or my PP?). In this case you take 5% less then the year before where the year before you took 4%, huh? I am missing something here.

Last edited by portart on Tue Nov 03, 2015 10:36 am, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

okay , day 1 of retirement you have 1 million clams saved .

you can start with a 40k paycheck first year .

next dec 31st you have an up year and have 1,200.000 .00 so your pay check is now 48k .

3rd year we have a bad year and you are back to 1 million on dec 31 .so you are going to take which ever is higher 4% of the million which is 40k or 48k less the 5% which is 45,600.00 . in this case 45,600 is higher and that is your new pay check for the year .

4th year you repeat and take nother 5% pay cut if need be .

the idea is this keeps you from having to take huge pay cuts if say we fall 40% . for your portfolio to survive only small cuts are needed with this method of withdrawals .

you can start with a 40k paycheck first year .

next dec 31st you have an up year and have 1,200.000 .00 so your pay check is now 48k .

3rd year we have a bad year and you are back to 1 million on dec 31 .so you are going to take which ever is higher 4% of the million which is 40k or 48k less the 5% which is 45,600.00 . in this case 45,600 is higher and that is your new pay check for the year .

4th year you repeat and take nother 5% pay cut if need be .

the idea is this keeps you from having to take huge pay cuts if say we fall 40% . for your portfolio to survive only small cuts are needed with this method of withdrawals .

Last edited by mathjak107 on Tue Nov 03, 2015 12:13 pm, edited 1 time in total.

Re: Why the PP is better in accumulation than you think

Let's say you literally retired two years ago, on November 2, 2013. From peaktotrough.com, with a portfolio of $1 million (and dividends reinvested), we get the following numbers:portart wrote: I am retiring in two years. I have the classic 25% PP. If I retired two years ago and drew out 4%, I am guessing I would down close to 8% since PP earned next to nothing in this time period. Assuming this is the case, what would I have to drop down to the the third year to avoid depleting my portfolio to the point that it would not come back to par as far as not outliving the money, assuming another 25 years of life? The original PP had money rates earning something in the 5% range. The money portion is now dead in the water with almost negative rates. Stocks and bonds keep the combination from outperforming enough to over come the shortfall in the cash portion. Gold is a wild card mainly for protection which can go many years before rebounding and can drop even futher due to its extreme volatility. What's everyone's take on this?

Initial values of stocks, bonds, cash, gold, and total PP:

11/2/2013: 250,000 250,000 250,000 250,000 1,000,000

After one year:

11/2/2014: 290,416 289,363 250,325 223,177 1,053,281

That's a gain of 5.3%. Withdrawing 4% from cash, that's $42,131, gives the following allocation:

11/2/2014: 290,416 289,363 208,194 223,177 1,011,150

The next year elapses:

11/2/2015: 307,067 303,056 208,714 215,414 1,034,251

That's a gain of 2.3%. Withdrawing 4% ($41,370) from cash gives:

11/2/2015: 307,067 303,056 167,344 215,414 992,881

Overall, you would be down less than 1% from your starting million. Would this return be worse from a different starting date? Perhaps. But we can see from this example that the PP hasn't been performing too badly recently.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

your master score card is this :

you need to maintain at least a 2% real return average for the first 15 years of a 30 year retirement to stand up to the traditional 4% safe withdrawal rate .

if you are getting less than that 7 years or so in you need to cut back the pay check .

if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

you need to maintain at least a 2% real return average for the first 15 years of a 30 year retirement to stand up to the traditional 4% safe withdrawal rate .

if you are getting less than that 7 years or so in you need to cut back the pay check .

if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: Why the PP is better in accumulation than you think

How much slack is there? Can you miss a couple or a string of years and make it up later before the 15th year, or MUST each and every year be at least 2% real return without exception?mathjak107 wrote: if you fail to get that 2% real return for the first 15 years then there will not be enough left to grow even if markets do turn around after that .

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

yes , in fact that is what will happen as sequence risk takes over . however being down for an extended period of time day 1 before an up cycle develops that cushion could seriously effect your outcome . the first 5 years can be pretty crucial to the success of the retirement while the first 15 determine the entire 30 year plus outcome .

follow that ?

this why methods like the rising glide path are now becoming popular to protect the early years when the most damage can be done .

follow that ?

this why methods like the rising glide path are now becoming popular to protect the early years when the most damage can be done .

Last edited by mathjak107 on Tue Nov 03, 2015 1:26 pm, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

keep in mind it isn't the size of the drop at all that hurts a retirement which is why draw down is a mental thing more than mathamatical . it is the length of time a recovery takes that is key .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , for a 2008 retiree it was a non event financially , perhaps not mentally because the recovery was so quick .

those who retired in 2008 are on track to be no different then any other retiree in any other normal time frame .

the y2k retiree is very different and they are on track to match the 1929 retiree which means income wise they will get through most likely but with very little left .

90% of the time retirees with a 50/50 mix or 60/40 following the 4% swr have ended with more than they started so the y2k retiree is on track to rival the 1929 retiree .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , for a 2008 retiree it was a non event financially , perhaps not mentally because the recovery was so quick .

those who retired in 2008 are on track to be no different then any other retiree in any other normal time frame .

the y2k retiree is very different and they are on track to match the 1929 retiree which means income wise they will get through most likely but with very little left .

90% of the time retirees with a 50/50 mix or 60/40 following the 4% swr have ended with more than they started so the y2k retiree is on track to rival the 1929 retiree .

Last edited by mathjak107 on Tue Nov 03, 2015 1:45 pm, edited 1 time in total.

Re: Why the PP is better in accumulation than you think

Both the size and duration of the drop matter. Unless you intentionally cut back your expenses in the down year (a fine idea, BTW), your fixed expenses (that do not shrink with your portfolio decline) will take out a large chunk of your investments and greatly prolong the recovery time to get back to where you were before. Drawdown complicates the recovery time, and volatility does have a measurable effect on withdrawal rates.mathjak107 wrote: keep in mind it isn't the size of the drop at all that hurts a retirement which is why draw down is a mental thing more than mathamatical . it is the length of time a recovery takes that is key .

even a modest drop for a couple of years can do damage which is why even the pp can be at risk as a retirement portfolio , 2008 was a non event because the recovery was so quick .

You're correct about the performance percentages of a 60/40 portfolio, and it's a fine choice in retirement. But using the same methodology other portfolios (including the PP) have supported higher withdrawal rates 100% of the time over the data we have available. One is free to choose the portfolio with the longer data set if that makes them feel more comfortable, but ignoring good opportunities simply because Ibbotson Associates didn't include those assets in their annual returns yearbook that the Trinity and Bengen studies used is up to the individual.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

Last edited by mathjak107 on Tue Nov 03, 2015 2:04 pm, edited 1 time in total.

-

dutchtraffic

- Executive Member

- Posts: 242

- Joined: Sat Apr 11, 2015 7:28 am

Re: Why the PP is better in accumulation than you think

You keep assuming things always recover within a year or so, clearly this is nonsense.

Now what..? US is replaying this scenario now.

Now what..? US is replaying this scenario now.

Re: Why the PP is better in accumulation than you think

From the Kitces paper (empahsis added):mathjak107 wrote: not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

He doesn't say the severity of the drop does not matter. Only that the recovery time also matters. I don't disagree with that at all. Also note that he's discussing the survival of a stock/bond portfolio (that I do not dispute), while I'm comparing performance of two different portfolios. Other portfolios he does not consider also do quite well while avoiding both the sharp and long declines.The viability of a 2008 retiree following the 4% rule is especially notable, and reflects a key (but often ignored or misunderstood) tenet of managing sequence-of-return risk in retirement: it’s actually not just about having a severe market crash in the early years of retirement, but a crash that doesn’t recover quickly.

Last edited by Tyler on Tue Nov 03, 2015 2:10 pm, edited 1 time in total.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

on the other hand the y2k retiree is the one in possible trouble .

Re: Why the PP is better in accumulation than you think

The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.mathjak107 wrote: well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

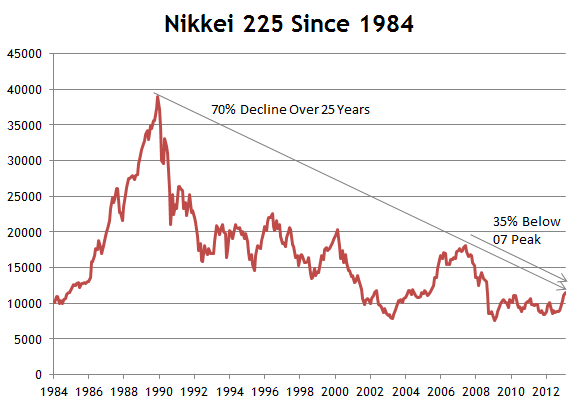

clearly we are not japan and have not been anything like japan in 30 years .dutchtraffic wrote: You keep assuming things always recover within a year or so, clearly this is nonsense.

Now what..? US is replaying this scenario now.

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

Tyler wrote:The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.mathjak107 wrote: well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..Tyler wrote:The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.mathjak107 wrote: well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

-

dutchtraffic

- Executive Member

- Posts: 242

- Joined: Sat Apr 11, 2015 7:28 am

Re: Why the PP is better in accumulation than you think

This is not an argument whatsoever.mathjak107 wrote: clearly we are not japan and have not been anything like japan in 30 years .

But you keep saying this, you really do believe americans are 'special' don't you..?

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

until our markets aren't , yes , we have been special and we are still one of the best places to invest in the world today - at least for now .

Re: Why the PP is better in accumulation than you think

Yes, they both were non-events in the sense that a 4% WR is working fine for both. The difference is that the low volatility (paired with reasonably high real returns) allows the PP to support a higher WR than the 60/40 portfolio over identical timeframes. That's what I mean about volatility making a difference. It's a big factor of what determines the SWR in the first place.mathjak107 wrote: correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

kitces:

The 2000 retiree is already half way through the 30-year time horizon with similar wealth to a 1929, 1937, or 1966 retiree had at this point, and the 2008 retiree is even further ahead than any of those historical scenarios (and even ahead of the 2000 retiree, too!).

And in the case of a 2008 retiree, the withdrawal rate is already right back at the 4% initial withdrawal rate the retiree began with (after already doing 6 years' worth of retirement spending!).

The 2000 retiree is already half way through the 30-year time horizon with similar wealth to a 1929, 1937, or 1966 retiree had at this point, and the 2008 retiree is even further ahead than any of those historical scenarios (and even ahead of the 2000 retiree, too!).

And in the case of a 2008 retiree, the withdrawal rate is already right back at the 4% initial withdrawal rate the retiree began with (after already doing 6 years' worth of retirement spending!).

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

i disagree , no way can you say the pp can support a higher withdrawal rate because if sequence risk and performance are less going forward the good years all portfolio's have end up paying for the bad years .Tyler wrote:Yes, they both were non-events in the sense that a 4% WR is working fine for both. The difference is that the low volatility (paired with reasonably high real returns) allows the PP to support a higher WR than the 60/40 portfolio over identical timeframes. That's what I mean about volatility making a difference. It's a big factor of what determines the SWR in the first place.mathjak107 wrote: correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..

i doubt the pp can claim that 90% of the time frames since 1926 30 years later the ending balance is more than you started with and 67% more than double left over .

first off you can't compare because of the gold issue pre 1975 .

if we rule out the two worst time frames a 60/40 mix has a 6.50% safe withdrawal rate and money left over .

Last edited by mathjak107 on Tue Nov 03, 2015 2:31 pm, edited 1 time in total.

-

dutchtraffic

- Executive Member

- Posts: 242

- Joined: Sat Apr 11, 2015 7:28 am

Re: Why the PP is better in accumulation than you think

Hahaha, you think Japan is some 3rd world country or something? Japan was an absolute powerhouse.mathjak107 wrote: until our markets aren't , yes , we have been special and we are still one of the best places to invest in the world today - at least for now .

"Throughout the 1970s, Japan had the world's third largest gross national product (GNP)—just behind the United States and Soviet Union— and ranked first among major industrial nations in 1990 in per capita GNP"

"Deflation in Japan started in the early 1990s. On 19 March 2001, the Bank of Japan and the Japanese government tried to eliminate deflation in the economy by reducing interest rates (part of their 'quantitative easing' policy). Despite having interest rates down near zero for a long period of time, this strategy did not succeed."

Hmm, where have we seen this before..

But oh wait, americans are immune to everything because they are "special"..right?

-

mathjak107

- Executive Member

- Posts: 4456

- Joined: Fri Jun 19, 2015 2:54 am

- Location: bayside queens ny

- Contact:

Re: Why the PP is better in accumulation than you think

japans central bank was clueless and 3x made tragic flaws that threw the country in to a deflationary spiral it can't break in 30 years .

while we are not invincible e are not japan .

while we are not invincible e are not japan .

Last edited by mathjak107 on Tue Nov 03, 2015 2:31 pm, edited 1 time in total.

-

dutchtraffic

- Executive Member

- Posts: 242

- Joined: Sat Apr 11, 2015 7:28 am

Re: Why the PP is better in accumulation than you think

So did the FED.

-

MachineGhost

- Executive Member

- Posts: 10054

- Joined: Sat Nov 12, 2011 9:31 am

Re: Why the PP is better in accumulation than you think

Here's the problem. The duration is out of your control unless you use downside risk management (whether that be trend following or adjusting portfolio duration). Are you 100% confident the government will everywhere and always always prop up the markets AND the public will not lose confidence in their actions being positive, as is now occuring in China and Japan?mathjak107 wrote: not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

BTW, when I judge what is risk-reward optimal in terms of drawdowns, I take into consideration BOTH the magnitude AND the duration. 1987 was deep but a blip and it will have a lower risk score than something like 2007-2009.

"All generous minds have a horror of what are commonly called 'Facts'. They are the brute beasts of the intellectual domain." -- Thomas Hobbes

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!

Disclaimer: I am not a broker, dealer, investment advisor, physician, theologian or prophet. I should not be considered as legally permitted to render such advice!