Page 8 of 9

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:10 pm

by mathjak107

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:12 pm

by Tyler

mathjak107 wrote:

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:13 pm

by mathjak107

dutchtraffic wrote:

You keep assuming things always recover within a year or so, clearly this is nonsense.

Now what..? US is replaying this scenario now.

clearly we are not japan and have not been anything like japan in 30 years .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:15 pm

by mathjak107

Tyler wrote:

mathjak107 wrote:

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.

Tyler wrote:

mathjak107 wrote:

well the 40% drop in 2008 was a non event , he says it . the fast recovery made it such .

on the other hand the y2k retiree is the one in possible trouble .

The 0.8% PP drop in 2008 was the true non-event. And a Y2k PP retiree is doing just fine.

correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:16 pm

by dutchtraffic

mathjak107 wrote:

clearly we are not japan and have not been anything like japan in 30 years .

This is not an argument whatsoever.

But you keep saying this, you really do believe americans are 'special' don't you..?

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:19 pm

by mathjak107

until our markets aren't , yes , we have been special and we are still one of the best places to invest in the world today - at least for now .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:20 pm

by Tyler

mathjak107 wrote:

correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..

Yes, they both were non-events in the sense that a 4% WR is working fine for both. The difference is that the low volatility (paired with reasonably high real returns) allows the PP to support a higher WR than the 60/40 portfolio over identical timeframes. That's what I mean about volatility making a difference. It's a big factor of what determines the SWR in the first place.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:20 pm

by mathjak107

kitces:

The 2000 retiree is already half way through the 30-year time horizon with similar wealth to a 1929, 1937, or 1966 retiree had at this point, and the 2008 retiree is even further ahead than any of those historical scenarios (and even ahead of the 2000 retiree, too!).

And in the case of a 2008 retiree, the withdrawal rate is already right back at the 4% initial withdrawal rate the retiree began with (after already doing 6 years' worth of retirement spending!).

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:25 pm

by mathjak107

Tyler wrote:

mathjak107 wrote:

correct but so is the conventionally invested retiree fine , it was the same non event for them as it was for the pp retiree ..

Yes, they both were non-events in the sense that a 4% WR is working fine for both. The difference is that the low volatility (paired with reasonably high real returns) allows the PP to support a higher WR than the 60/40 portfolio over identical timeframes. That's what I mean about volatility making a difference. It's a big factor of what determines the SWR in the first place.

i disagree , no way can you say the pp can support a higher withdrawal rate because if sequence risk and performance are less going forward the good years all portfolio's have end up paying for the bad years .

i doubt the pp can claim that 90% of the time frames since 1926 30 years later the ending balance is more than you started with and 67% more than double left over .

first off you can't compare because of the gold issue pre 1975 .

if we rule out the two worst time frames a 60/40 mix has a 6.50% safe withdrawal rate and money left over .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:27 pm

by dutchtraffic

mathjak107 wrote:

until our markets aren't , yes , we have been special and we are still one of the best places to invest in the world today - at least for now .

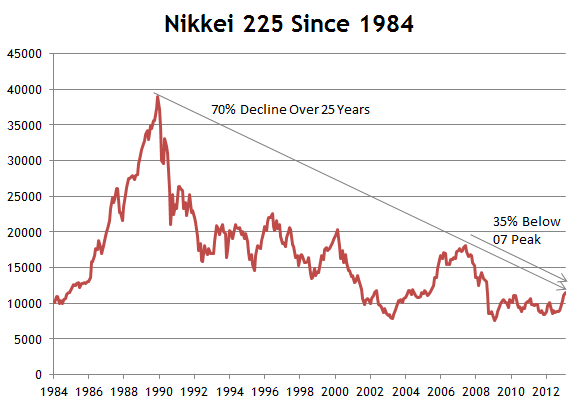

Hahaha, you think Japan is some 3rd world country or something? Japan was an absolute powerhouse.

"Throughout the 1970s, Japan had the world's third largest gross national product (GNP)—just behind the United States and Soviet Union— and ranked first among major industrial nations in 1990 in per capita GNP"

"Deflation in Japan started in the early 1990s. On 19 March 2001, the Bank of Japan and the Japanese government tried to eliminate deflation in the economy by reducing interest rates (part of their 'quantitative easing' policy). Despite having interest rates down near zero for a long period of time, this strategy did not succeed."

Hmm, where have we seen this before..

But oh wait, americans are immune to everything because they are "special"..right?

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:29 pm

by mathjak107

japans central bank was clueless and 3x made tragic flaws that threw the country in to a deflationary spiral it can't break in 30 years .

while we are not invincible e are not japan .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:31 pm

by dutchtraffic

So did the FED.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:35 pm

by MachineGhost

mathjak107 wrote:

not quite true about steep drops , michael kitces did a paper on this . it is only the duration . a steep drop like 2008 was a non event to its success rate .. a modest drop over an extended duration has far more serious consequences .

the worst case scenario's the 4% safe withdrawal rate is based on already expects steep drops . that is why it is called a safe withdrawal rate . all it cares about is the 15 year average is at least a 2% real return .

https://www.kitces.com/blog/how-has-the ... al-crisis/

Here's the problem. The duration is out of your control unless you use downside risk management (whether that be trend following or adjusting portfolio duration). Are you 100% confident the government will everywhere and always always prop up the markets AND the public will not lose confidence in their actions being positive, as is now occuring in China and Japan?

BTW, when I judge what is risk-reward optimal in terms of drawdowns, I take into consideration BOTH the magnitude AND the duration. 1987 was deep but a blip and it will have a lower risk score than something like 2007-2009.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:37 pm

by mathjak107

we are never sure of much when it come to investing , but one thing seems pretty sure and that is out of all the timing systems out there including the failed market timing graveyard i don't know of any that passed any academic study as far as working long enouh to be of use .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:39 pm

by MachineGhost

mathjak107 wrote:

The 2000 retiree is already half way through the 30-year time horizon with similar wealth to a 1929, 1937, or 1966 retiree had at this point, and the 2008 retiree is even further ahead than any of those historical scenarios (and even ahead of the 2000 retiree, too!).

Pretty much a solid argument there for using downside risk management. 2008 was the exception to the rule due to QEternity. Betting on exceptions to repeat is foolish.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:40 pm

by mathjak107

betting this time is different has been even more foolish and costly .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:41 pm

by Tyler

mathjak107 wrote:

i disagree , no way can you say the pp can support a higher withdrawal rate because if sequence risk and performance are less going forward the good years all portfolio's have end up paying for the bad years .

i doubt the pp can claim that 90% of the time frames since 1926 30 years later the ending balance is more than you started with and 67% more than double left over .

first off you can't compare because of the gol issue pre 1975 .

Well I've provided tools to compare both portfolios since 1972. The relative SWR performance of the PP vs the 60/40 over the same timeframe is quite clear, with the PP supporting a significantly higher WR. The absolute SWR throughout all of history is certainly up for debate, and the longer back you look the lower it will be. I see no evidence, however, that if you look back to 1926 (and if the gold standard laws were the same then) the PP will look significantly worse while the 60/40 will not (the 60/40 SWR since 1972 is only 0.3% higher than the one since 1870). So I believe one can make an educated decision on the relative merits with the data provided, and conservatively plan to reduce the absolute WR to account for longer timeframes. You may disagree, and prefer to only invest in portfolios with data going back to 1926. Either approach is fine, IMHO. In the end, we all have to be comfortable with our plan.

For the record, I think the 60/40 portfolio is a fine choice. I just find the myopic focus on the S&P500 and total bond market to be pretty darn boring and shortsighted. The investing world is a lot more interesting than that, and other portfolios may have different results. Including your own Mathjak portfolio!

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:42 pm

by mathjak107

as long as we are making up what our perception of us gold prices would be make sure you use 35 bucks an ounce too , it will really shine .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:44 pm

by MachineGhost

mathjak107 wrote:

we are never sure of much when it come to investing , but one thing seems pretty sure and that is out of all the timing systems out there including the failed market timing graveyard i don't know of any that passed any academic study as far as working long enouh to be of use .

I'll post them for you when I come across them again. But there's many other downside risk management approaches that work to beat buy and hold besides just trend following. There's trailing stops, there's rebalancing bands, there's modifying portfolio duration, there's constant proportion portfolio insurance, there's dollar cost averaging, there's the reverse glide path, etc. Not all of these have formal academic evidence even though they work empirically. Waiting for academics to catch up to the real world is how a lot of money is left on the table. Academics are 1) not investors and 2) not traders.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:52 pm

by mathjak107

the proof will be in the pudding as they say ,.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 2:57 pm

by ochotona

mathjak107 wrote:

the proof will be in the pudding as they say ,.

The proof will be in the backtesting? But I though you said that backtesting was...

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 3:01 pm

by mathjak107

nope , the proof will be going forward and how "you " do . afterall that is all that counts .

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 3:07 pm

by Jack Jones

Tyler wrote:

For the record, I think the 60/40 portfolio is a fine choice. I just find the myopic focus on the S&P500 and total bond market to be pretty darn boring and shortsighted. The investing world is a lot more interesting than that, and other portfolios may have different results.

I sometimes feel the same way about the PP. In light of the old saying, "diversification is the only free lunch", sometimes I feel like we're leaving some food on the table in the form of international assets, real estate, commodities, etc.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 3:10 pm

by ochotona

Jack Jones wrote:

Tyler wrote:

For the record, I think the 60/40 portfolio is a fine choice. I just find the myopic focus on the S&P500 and total bond market to be pretty darn boring and shortsighted. The investing world is a lot more interesting than that, and other portfolios may have different results.

I sometimes feel the same way about the PP. In light of the old saying, "diversification is the only free lunch", sometimes I feel like we're leaving some food on the table in the form of international assets, real estate, commodities, etc.

Ivy-5 has US stocks, ex-US stocks, REITs, bonds, commodities. Tyler has coded it as one of default lazy portfolios.

Re: Why the PP is better in accumulation than you think

Posted: Tue Nov 03, 2015 3:23 pm

by Jack Jones

ochotona wrote:

Jack Jones wrote:

I sometimes feel the same way about the PP. In light of the old saying, "diversification is the only free lunch", sometimes I feel like we're leaving some food on the table in the form of international assets, real estate, commodities, etc.

Ivy-5 has US stocks, ex-US stocks, REITs, bonds, commodities. Tyler has coded it as one of default lazy portfolios.

I know.

I've been reading a lot of Faber's stuff recently. I just got a free ebook (Global Asset Allocation) from him. There's a section on the PP, but I haven't read it yet.