Treasury Bond Buying Tutorial

Moderator: Global Moderator

-

mandynshane

Re: Treasury Bond Buying Tutorial

anyone know anything about treasury direct?

Re: Treasury Bond Buying Tutorial

Thank you Gumby.

Vanguard's bond desk is almost as easy to use as well (but Fidelity's interface looks amazingly simple and others should learn from it). Buying bonds is not hard and is what I do myself and recommend if you are able. They just sit there and pay interest once this is all done.

Thanks again Gumby!

Vanguard's bond desk is almost as easy to use as well (but Fidelity's interface looks amazingly simple and others should learn from it). Buying bonds is not hard and is what I do myself and recommend if you are able. They just sit there and pay interest once this is all done.

Thanks again Gumby!

Last edited by craigr on Fri Oct 28, 2011 2:48 pm, edited 1 time in total.

Re: Treasury Bond Buying Tutorial

Well done!

I use this myself and can verify that it's just as easy as it looks. In fact, I use these screens to purchase individual T-bills and T-notes to construct a ladder for the "cash" portion of the portfolio. That covers both "cash" and "bonds".

If you find yourself a nice, safe place for physical bullion (like a cheap safe deposit box), you're looking at direct ownership and a 0% expense ratio for the great majority of your portfolio. There's a lot to like about that.

I use this myself and can verify that it's just as easy as it looks. In fact, I use these screens to purchase individual T-bills and T-notes to construct a ladder for the "cash" portion of the portfolio. That covers both "cash" and "bonds".

If you find yourself a nice, safe place for physical bullion (like a cheap safe deposit box), you're looking at direct ownership and a 0% expense ratio for the great majority of your portfolio. There's a lot to like about that.

Re: Treasury Bond Buying Tutorial

0% expense for 50% of the PP in the form of LT and ST treasuries.Lone Wolf wrote: If you find yourself a nice, safe place for physical bullion (like a cheap safe deposit box), you're looking at direct ownership and a 0% expense ratio for the great majority of your portfolio. There's a lot to like about that.

0% expense for 25% of the PP in the form of safe deposit box at neighborhood bank that provides the box free to longtime customers.

Tiny expense ratio for stock market index fund.

It's one more thing to like about the PP.

Q: “Do you have funny shaped balloons?”

A: “Not unless round is funny.”

A: “Not unless round is funny.”

Re: Treasury Bond Buying Tutorial

I think we should mention the implied "load" of gold buying (I'll leave treasury-buying out since Fidelity allows it for free).

Also storage or insurance on physical gold should also be added as another small asterisk.

Just playing devil's advocate. I fully agree with MT that the cheapness is stunning.

Also storage or insurance on physical gold should also be added as another small asterisk.

Just playing devil's advocate. I fully agree with MT that the cheapness is stunning.

"Men did not make the earth. It is the value of the improvements only, and not the earth itself, that is individual property. Every proprietor owes to the community a ground rent for the land which he holds."

- Thomas Paine

- Thomas Paine

Re: Treasury Bond Buying Tutorial

True! Still, this is only a one-time charge and (if you shop around) not a terribly big one. For example, Tulving's offering Maple Leaf coins for $35 over spot and buying them back for $17 over spot. That's an $18 spread per coin, so just a hair over 1%. Not much in the scheme of things if you hold your gold for a long time.moda0306 wrote: I think we should mention the implied "load" of gold buying (I'll leave treasury-buying out since Fidelity allows it for free).

Also, if you're macho enough (and rich enough!), get yourself a 1 kilo gold bar for straight-up spot.

Insurance may not be a bad way to spend some of your PP riches but it's not a requirement. Storage in a safe deposit box at your local bank is cheap, often around $30-$50 per year. If you hold even 20 ounces of gold in a $30 safe deposit box, that works out to less than 0.08% per year.moda0306 wrote: Also storage or insurance on physical gold should also be added as another small asterisk.

Re: Treasury Bond Buying Tutorial

Not a problem. And thank you for shedding light on some of the questionable practices of Treasury bond funds.craigr wrote: Thank you Gumby.

Vanguard's bond desk is almost as easy to use as well (but Fidelity's interface looks amazingly simple and others should learn from it). Buying bonds is not hard and is what I do myself and recommend if you are able. They just sit there and pay interest once this is all done.

Thanks again Gumby!

Craigr, I noticed that you posted a link to this tutorial. That's great. However, if you, or anyone else, wants to copy/share this tutorial to your own site, you should feel free to do so. Copy the text and photos, and/or edit the text. Do whatever you like. That's why I made it. Knowledge is power and this kind of knowledge should really be shared and copied with as many people as possible so that people can take their finances into their own hands.

Nothing I say should be construed as advice or expertise. I am only sharing opinions which may or may not be applicable in any given case.

Re: Treasury Bond Buying Tutorial

It's worth noting that the very same process can be used to buy short term treasuries at auction to set up a ladder with whatever duration you want with as many rungs as you want instead of relying on a treasury MM or ETF such as SHY for your cash as well. Fidelity even has an "auto roll" feature where you can sign up to have the principal for maturing bonds automatically reinvested in bonds of the same term. If you set up, say, a 2-year ladder with 8 rungs then 1/8th of your cash in this ladder matures every 3 months. With auto-roll, if you do nothing then every three months 1/8th of your cash simply rolls over into another 2 year bond (bought at auction). If you need some cash for rebalancing or any other reason, you can prevent the auto-roll from happening and when the bond matures the principal is deposited in your brokerage cash account. You can do the same thing through TreasuryDirect as well. See

-

dualstow

- Executive Member

- Posts: 15308

- Joined: Wed Oct 27, 2010 10:18 am

- Location: searching for the lost Xanadu

- Contact:

Re: Treasury Bond Buying Tutorial

Brilliant work, Gumby!

I use Fidelity for long bonds, too, since my 401(k) is there. For those of you who buy at auction like I do, I will add that you can sign up for email alerts about new offerings. The email looks like this:

I use Fidelity for long bonds, too, since my 401(k) is there. For those of you who buy at auction like I do, I will add that you can sign up for email alerts about new offerings. The email looks like this:

Link: https://www.fidelity.com/fixed-income-b ... ols/alertsFidelity is pleased to announce the possibility for Brokerage customers to participate in next week’s U.S. Treasury Note/Bond Auction(s):

UST Maturing 01/26/2012 Auction Close Date: 10/24/2011

UST Maturing 04/26/2012 Auction Close Date: 10/24/2011

UST Maturing 10/31/2013 Auction Close Date: 10/25/2011

UST Maturing 10/31/2016 Auction Close Date: 10/26/2011

UST Maturing 10/31/2018 Auction Close Date: 10/27/2011

RIP LALO SCHIFRIN

Re: Treasury Bond Buying Tutorial

I sold about 80% of my TLT today at the market open, and I have an internal conflict. With the bulk of my long bonds liquidated, I feel as if my left flank is uncovered as I have the three business days before I can buy bonds. On the other hand, and I realize that I am violating the code here, but, I am extraordinarily tempted to market time or dollar cost average my move back in.

What would you do?

What would you do?

Re: Treasury Bond Buying Tutorial

When you covert your TLT to cash, you've effectively turned 50% of your portfolio into cash. So, a portfolio consisting of (roughly) 50% cash, 25% stocks and 25% gold probably isn't going to be all that different from a traditional 4x25 PP over the span of three days. That's because you've basically turned your portfolio into a version of PRPFX (which can't own very many Long Term Bonds). Actually, your portfolio will most closely resemble Clive's "Rate Tart" PP — which held up very well through 2008-2009. The only difference between the "Rate Tart" PP and the 4x25 PP was that the 4x25 PP recovered more quickly in Dec 2008, when the LTTs kicked in big time.6 Iron wrote: I sold about 80% of my TLT today at the market open, and I have an internal conflict. With the bulk of my long bonds liquidated, I feel as if my left flank is uncovered as I have the three business days before I can buy bonds. On the other hand, and I realize that I am violating the code here, but, I am extraordinarily tempted to market time or dollar cost average my move back in.

What would you do?

http://gyroscopicinvesting.com/forum/ht ... 730#p12730

(Keep in mind that Clive's comments are deleted from the "Rate Tart" PP discussion)

So, you can probably relax more than you think. But, my recommendation is still to buy your bonds sooner rather than later, since we may be experiencing some high volatility in the next few weeks as Greece appears to move closer and closer to its eventual default. Do what feels right, but know that it probably won't make a tremendous difference either way.

Last edited by Gumby on Wed Nov 02, 2011 12:02 am, edited 1 time in total.

Nothing I say should be construed as advice or expertise. I am only sharing opinions which may or may not be applicable in any given case.

Re: Treasury Bond Buying Tutorial

Gumby, thank you very much for posting your tutorial. Now I feel ashamed that I've been with Fidelity for a long time and never even thought about the bond buying feature. In fact, I always thought that directly buying bonds is something very complicated and costly. And now I feel enlightened.

A couple of questions came to my mind after reading your post:

1. Market order vs. limit order: does it really matter which type of order to use?

2. Is it better to use a ladder of bonds spreading the purchases in time or just sell all my EDV/TLT and buy bonds at once?

3. What is the difference between buying at the auction or secondary market?

A couple of questions came to my mind after reading your post:

1. Market order vs. limit order: does it really matter which type of order to use?

2. Is it better to use a ladder of bonds spreading the purchases in time or just sell all my EDV/TLT and buy bonds at once?

3. What is the difference between buying at the auction or secondary market?

Last edited by foglifter on Wed Nov 02, 2011 1:19 pm, edited 1 time in total.

"Let every man divide his money into three parts, and invest a third in land, a third in business, and a third let him keep in reserve."

- Talmud

- Talmud

Re: Treasury Bond Buying Tutorial

I would also like to know what the advantage of buying at auction is. It seems like you'd get slippage due to the multi-day difference between the auction close and the issue date.

I'm currently looking at Fidelity and trying to choose between two secondary-market options:

Name: UNITED STATES TREAS BDS

Coupon: 4.37500%

Maturity: 05/15/2041

Price: 126.687 / 126.781

Yield: 3.005 / 3.001

Quantity: 1,000(1) / 1,000 (1)

Name: UNITED STATES TREAS BDS

Coupon: 3.75000%

Maturity: 08/15/2041

Price: 114.125 / 114.172

Yield: 3.027 / 3.024

Quantity: 999(1) / 999 (1)

So what's causing the difference in yield? Is it really the extra 3 months, or $1 difference in quantity? I was going to grab some of the second, but it's clear I don't completely understand how bond buying works (I have TLT now)

Edit: OK, now that I've logged in I can see the images and this question has been addressed (kind of). People are paying more for the higher coupon, even though the effective yield is therefore lower? That seems kind of silly.

I'm currently looking at Fidelity and trying to choose between two secondary-market options:

Name: UNITED STATES TREAS BDS

Coupon: 4.37500%

Maturity: 05/15/2041

Price: 126.687 / 126.781

Yield: 3.005 / 3.001

Quantity: 1,000(1) / 1,000 (1)

Name: UNITED STATES TREAS BDS

Coupon: 3.75000%

Maturity: 08/15/2041

Price: 114.125 / 114.172

Yield: 3.027 / 3.024

Quantity: 999(1) / 999 (1)

So what's causing the difference in yield? Is it really the extra 3 months, or $1 difference in quantity? I was going to grab some of the second, but it's clear I don't completely understand how bond buying works (I have TLT now)

Edit: OK, now that I've logged in I can see the images and this question has been addressed (kind of). People are paying more for the higher coupon, even though the effective yield is therefore lower? That seems kind of silly.

Last edited by dragoncar on Wed Nov 02, 2011 2:06 pm, edited 1 time in total.

Re: Treasury Bond Buying Tutorial

Why can't you buy bonds now?6 Iron wrote: I sold about 80% of my TLT today at the market open, and I have an internal conflict. With the bulk of my long bonds liquidated, I feel as if my left flank is uncovered as I have the three business days before I can buy bonds. On the other hand, and I realize that I am violating the code here, but, I am extraordinarily tempted to market time or dollar cost average my move back in.

What would you do?

Re: Treasury Bond Buying Tutorial

dragoncar, The lower coupon one will have a longer duration (ie be more volatile) because of the lower coupon. It is further towards the spectrum of being like a zero coupon such as in EDV. Most people see that as a problem but for us PPs it is an advantage. The longer duration one gets the higher yield because most people dont like long duration (that is why the 30y has better yield than 10y most of the time). The second one is the best for the PP IMO. There are online duration calculators you can use. On the whole just going for the longest duration is best.

"Good judgment comes from experience. Experience comes from bad judgment." - Mulla Nasrudin

Re: Treasury Bond Buying Tutorial

Thanks, Stone... although I understand the fundamental of how a bond works, I obviously need to do more research on how the bond market works -- I had forgotten about the duration calculation.

Thanks also to Gumby for the tutorial. One note that was still confusing to me: What exactly does the "price" mean? For example, Fidelity may give you a confirmation screen that looks like this:

Price: $114.00

Quantity: 10,000.00

Total: $11,400.00

It seems like the total should = quantity * price. However, if you enter "10" into the quantity, the total will be quantity * 10 * price. Is it just convention to list the price as 1/10 of the actual price?

Thanks also to Gumby for the tutorial. One note that was still confusing to me: What exactly does the "price" mean? For example, Fidelity may give you a confirmation screen that looks like this:

Price: $114.00

Quantity: 10,000.00

Total: $11,400.00

It seems like the total should = quantity * price. However, if you enter "10" into the quantity, the total will be quantity * 10 * price. Is it just convention to list the price as 1/10 of the actual price?

Re: Treasury Bond Buying Tutorial

I can, but not with the proceeds of the sale of TLT until it clears. I suppose that I could have moved cash positions into the trading account but that seemed cumbersome, and I thought I would wait. Of course, that means that Greece and the Euro will go into a nosedive tomorrow.dragoncar wrote:Why can't you buy bonds now?6 Iron wrote: I sold about 80% of my TLT today at the market open, and I have an internal conflict. With the bulk of my long bonds liquidated, I feel as if my left flank is uncovered as I have the three business days before I can buy bonds. On the other hand, and I realize that I am violating the code here, but, I am extraordinarily tempted to market time or dollar cost average my move back in.

What would you do?

Re: Treasury Bond Buying Tutorial

Oh, I saw you say something about settling time, but I didn't understand. Fidelity is cool with using unsettled funds to buy. You just can't "freeride" by then selling the new securities before the funds with which you bought them settle. Examples:6 Iron wrote:I can, but not with the proceeds of the sale of TLT until it clears. I suppose that I could have moved cash positions into the trading account but that seemed cumbersome, and I thought I would wait. Of course, that means that Greece and the Euro will go into a nosedive tomorrow.dragoncar wrote:

Why can't you buy bonds now?

Sell tlt, buy bonds same day: ok (I just did this in my Roth Ira)

Sell tlt, buy bonds same day, sell bonds next day: freeriding (I think you just get a warning though the first time)

Re: Treasury Bond Buying Tutorial

It depends on what you want. If you know what price you want to pay for the bonds — and don't mind waiting for the market to hit that price — then use a limit order. If you just want the bonds now — and don't mind paying the market price — use a market order. With a market order, you are going to pay something close to the latest "Ask" price. However, with a limit order, you risk not getting the bonds at all if the market price rises from that point forward. I have also used market orders for Treasuries many times and never been disappointed. So, it really depends on what you want and how much you're willing to spend.foglifter wrote: A couple of questions came to my mind after reading your post:

1. Market order vs. limit order: does it really matter which type of order to use?

One easy way to decide is to look at the Bid/Ask spread. Since the Treasury market is very liquid, the Bid/Ask spread is almost always very tight. In other words, the bidder's price will almost always be extremely close to the asker's price. When you place a market order, you are basically saying that you're willing to take the "Ask" price, whatever it may be. With Treasuries, I don't think it really matters because of the liquidity and the spread is almost always going to be very tight.

Keep in mind that retail brokerages don't put you at the front of the line when limit trades happen. Most of these brokerage houses will usually only sell you something as a limit order if the price drops a few pennies below your bid price, because they will typically try to buy for a slight discount and then quickly sell it to you for the price you asked for. This is even true in full-service brokerage houses — and it's been a long-standing tradition on Wall Street. Remember, most people on Wall Street make most of their money through billions and billions of pennies that add up.

However, I would definitely recommend that you use a limit order when selling your bonds. That way you get the price that you want.

If you're unhappy with TLT, just sell it and buy 30 year Treasuries all at once. Your 20-30 year ladder will happen gradually over time as you rebalance into bonds over the years. The truth is that if taxes (and simplicity) weren't a factor you're PP might actually be better off rolling over 29 year Treasuries back into 30 year Treasuries each year. But, for the sake of our sanity, we just let a natural ladder happen on its own. There are some advantages to having a naturally occurring 20-30 year ladder in your pocket. For example, if you ever have a capital gain in another asset, like your Stocks, you might be able to sell a losing 23 year Treasury — take a capital loss, for tax loss harvesting — and roll it over to a new 30-year Treasury without any wash sale issues (since the durations are so different). Of course, that's just a futuristic hypothetical situation (since a seven-year-old 2034 Treasury should be doing pretty well right now).foglifter wrote:2. Is it better to use a ladder of bonds spreading the purchases in time or just sell all my EDV/TLT and buy bonds at once?

In terms of the actual bond, there is no difference whatsoever — since the bonds themselves are just electronic records in your account. Some brokerage houses will charge a fee to transact with the secondary market. But, at Fidelity, they are free either way. So, it makes no difference at Fidelity or Schwab. If you want the bonds immediately, just buy them on the secondary market.foglifter wrote:3. What is the difference between buying at the auction or secondary market?

If you happen to be just a day or two away from the regularly scheduled 30 year auction, you may want to participate in the auction just for fun. Just understand that you will be entering a "non-competitive" bid at the auction — which means that you are willing to pay the market price, for that bond, at the time of auction. If the auction isn't as highly over-subscribed as it usually is, you may get a nice little discount at the auction (maybe something like $999 per bond) — which is always fun. And the level of participation in the auction will typically affect the mood of the bond market. But, it's probably not worth waiting a week or two just to participate in the auction.

So, the secondary market is where all the trading action is. The auction is where the bonds are handed out to the public for trading and holding. After the auction is complete and the accounts are settled, most of those new bonds will be trading on the secondary market anyway — and that's why the Treasury market is so liquid.

Bottom line...if your brokerage house isn't going to charge you anything to participate in the secondary market, you'll have more control in the secondary market. And, of course, remember that you can only sell your bonds on the secondary market. The auction is really for those who want to have a little fun with it.

Last edited by Gumby on Thu Nov 03, 2011 11:03 am, edited 1 time in total.

Nothing I say should be construed as advice or expertise. I am only sharing opinions which may or may not be applicable in any given case.

Re: Treasury Bond Buying Tutorial

So... the 30-year Treasury Auction happened at 1PM today, and if you were lucky enough to have taken part in it, you got in at a nice discount. Why? Because the 30-year auction had disappointing results since it didn't have as many bidders as it normally does. It was "only" oversubscribed by 2.40:1 (versus the 2.94:1 Bid-to-Cover Ratio from last month). The Primary Dealers (the banks that help make the Treasury market more liquid) had to pick up a greater share of the slack from the weak public reception — as their Fed contract requires them to do.

http://www.treasurydirect.gov/instit/an ... 1110_1.pdf

I wouldn't read too much into the weak public reception. There are a lot of things happening in the bond market that would have attracted money away from the 30-year auction.

In any case, you can see the moment when the results were released as TLT (the blue line), instantly tracked the temporary spike in yields...

[align=center] [/align]

[/align]

And as you can see, the dip was temporary — nothing more than a welcome blip for those who took part in the auction.

In recent months, the Treasury auctions have provided a nice little discount to Long Term Treasury buyers. But, my feeling is that the auction doesn't necessarily help you if you end up needing the bonds sooner than the auction schedule allows, since market conditions can often change a lot in between auction dates.

Still, congrats to those who took part in the auction.

http://www.treasurydirect.gov/instit/an ... 1110_1.pdf

I wouldn't read too much into the weak public reception. There are a lot of things happening in the bond market that would have attracted money away from the 30-year auction.

In any case, you can see the moment when the results were released as TLT (the blue line), instantly tracked the temporary spike in yields...

[align=center]

[/align]And as you can see, the dip was temporary — nothing more than a welcome blip for those who took part in the auction.

In recent months, the Treasury auctions have provided a nice little discount to Long Term Treasury buyers. But, my feeling is that the auction doesn't necessarily help you if you end up needing the bonds sooner than the auction schedule allows, since market conditions can often change a lot in between auction dates.

Still, congrats to those who took part in the auction.

Last edited by Gumby on Thu Nov 10, 2011 3:13 pm, edited 1 time in total.

Nothing I say should be construed as advice or expertise. I am only sharing opinions which may or may not be applicable in any given case.

Re: Treasury Bond Buying Tutorial

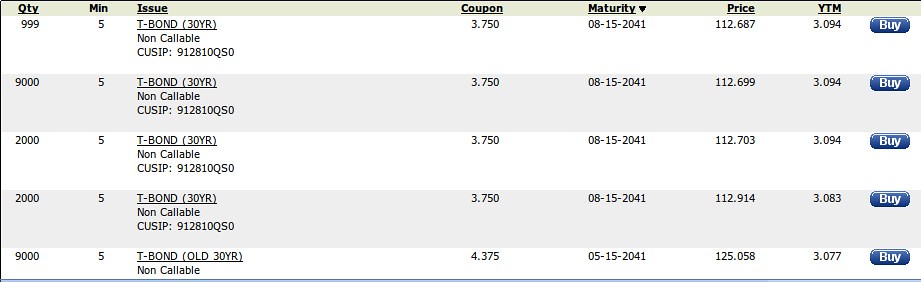

Gumby, thanks very much for this guide. I hold TLT in a Scottrade Roth IRA and am now considering buying the bonds themselves instead, but I don't quite understand how it works at Scottrade. I guess Scottrade acts as principal and thus marks the bonds up a bit for investors who wish to buy. Here is an example of Scottrade's Treasury bond offerings today:

So comparing the 8/15/2041 maturity price to the bid/ask of 112.3594/112.4375 taken from http://online.wsj.com/mdc/public/page/2 ... asury.html it looks like the markup is roughly 0.27% Then to buy $100,000 worth of these bonds would cost around $270, which is almost enough to make me consider moving to Fidelity if indeed they offer this service for free.

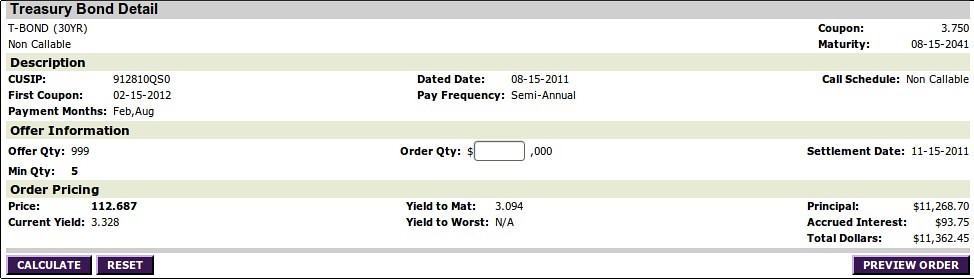

Clicking the first 8/15/2041 bond "Buy" link gives this

which is where it gets confusing to me. First of all, are these $10,000 bonds? Secondly, am I paying for accrued interest in some way? Thirdly, why is the order quantity in dollars?

And this is just the buying process, I'm not sure at all how selling works.

I suppose I should just give them a call on Monday to hold my hand through the process.

So comparing the 8/15/2041 maturity price to the bid/ask of 112.3594/112.4375 taken from http://online.wsj.com/mdc/public/page/2 ... asury.html it looks like the markup is roughly 0.27% Then to buy $100,000 worth of these bonds would cost around $270, which is almost enough to make me consider moving to Fidelity if indeed they offer this service for free.

Clicking the first 8/15/2041 bond "Buy" link gives this

which is where it gets confusing to me. First of all, are these $10,000 bonds? Secondly, am I paying for accrued interest in some way? Thirdly, why is the order quantity in dollars?

And this is just the buying process, I'm not sure at all how selling works.

I suppose I should just give them a call on Monday to hold my hand through the process.

Oh, such a beautiful tarmac. Look how smooth it is. See how smooth it is? And it's warm, and it's hard. - Charley Boorman Long Way Round

Re: Treasury Bond Buying Tutorial

The minimum denomination is $1,000 at Fidelity

https://www.fidelity.com/bonds/us-treasury-bonds

...Your screenshot seems to imply that the denomination at Scottrade is $1,000 as well. (I believe you can buy the bonds in $100 denominations on TreasuryDirect, so that's probably why the official market price is quoted near $100). Clicking "Calculate" should provide some clues. But, you should call Scottrade's Bond Desk up and they will let you know for sure. I'm sure they will be able to clear it all up for you. When in doubt, always call up the bond desk and ask.

Unless I'm missing something, it's difficult to tell if the markup is as high as you suspect it is. The WSJ link suggests that the quotes were calculated at 3PM. Unless your screenshot was taken at 3PM, I'm not sure you can really come to any conclusions.

Your best bet is to call them up if you have questions.

https://www.fidelity.com/bonds/us-treasury-bonds

...Your screenshot seems to imply that the denomination at Scottrade is $1,000 as well. (I believe you can buy the bonds in $100 denominations on TreasuryDirect, so that's probably why the official market price is quoted near $100). Clicking "Calculate" should provide some clues. But, you should call Scottrade's Bond Desk up and they will let you know for sure. I'm sure they will be able to clear it all up for you. When in doubt, always call up the bond desk and ask.

Unless I'm missing something, it's difficult to tell if the markup is as high as you suspect it is. The WSJ link suggests that the quotes were calculated at 3PM. Unless your screenshot was taken at 3PM, I'm not sure you can really come to any conclusions.

Your best bet is to call them up if you have questions.

Last edited by Gumby on Fri Nov 11, 2011 10:54 pm, edited 1 time in total.

Nothing I say should be construed as advice or expertise. I am only sharing opinions which may or may not be applicable in any given case.

Re: Treasury Bond Buying Tutorial

3pm Thursday was the last time bonds were traded, which explains the time stamp on the quotes I believe. The $11,000 numbers were confusing me, and I think you're right about them being $1,000 bonds. The numbers quoted in the image seem to have been for a default value of 10 bonds. Any integer input into the form along with "Calculate" gives the expected result. Still don't understand the accrued interest, but I'll take that up with customer service.

Oh, such a beautiful tarmac. Look how smooth it is. See how smooth it is? And it's warm, and it's hard. - Charley Boorman Long Way Round

Re: Treasury Bond Buying Tutorial

I've given up on the idea of trading treasury bonds in my Scottrade Roth IRA and have transferred the assets to a Fidelity Roth IRA. I'm about to sell TLT and buy bonds, and just wanted to make sure there was no reason to avoid the just-issued 11/15/2041 maturity treasury bonds - CUSIP 912810QT8. For the purposes of the Permanent Portfolio, they are just fine?

Oh, such a beautiful tarmac. Look how smooth it is. See how smooth it is? And it's warm, and it's hard. - Charley Boorman Long Way Round

Re: Treasury Bond Buying Tutorial

Just bought some myself. For the LT's buy the longest dated ones you can IMO.

You pay accrued interest, when you buy. That is the interest that has accumulated since the last coupon payment. When the coupon comes due, you get the full interest payment, so you get that money back at that time. On the other side of the trade, the seller gets that accrued interest for the time he has held the bond since the last interest payment.

The 11/15 Bond pays in May 15 and Nov 15, so right now there is not much accrued interest.

When I value my bond and note holdings, I add in the accrued interest, since that would be what I would receive if I sold them.

You pay accrued interest, when you buy. That is the interest that has accumulated since the last coupon payment. When the coupon comes due, you get the full interest payment, so you get that money back at that time. On the other side of the trade, the seller gets that accrued interest for the time he has held the bond since the last interest payment.

The 11/15 Bond pays in May 15 and Nov 15, so right now there is not much accrued interest.

When I value my bond and note holdings, I add in the accrued interest, since that would be what I would receive if I sold them.

ZedThou wrote: I've given up on the idea of trading treasury bonds in my Scottrade Roth IRA and have transferred the assets to a Fidelity Roth IRA. I'm about to sell TLT and buy bonds, and just wanted to make sure there was no reason to avoid the just-issued 11/15/2041 maturity treasury bonds - CUSIP 912810QT8. For the purposes of the Permanent Portfolio, they are just fine?

Last edited by SteveGo on Thu Nov 17, 2011 10:09 am, edited 1 time in total.

Steve G