ochotona wrote: ↑Sun Jan 20, 2019 3:02 pm

Awful. One of you please start a real HBPP ETF and charge 10 basis points above the costs of the underlying ETFs.

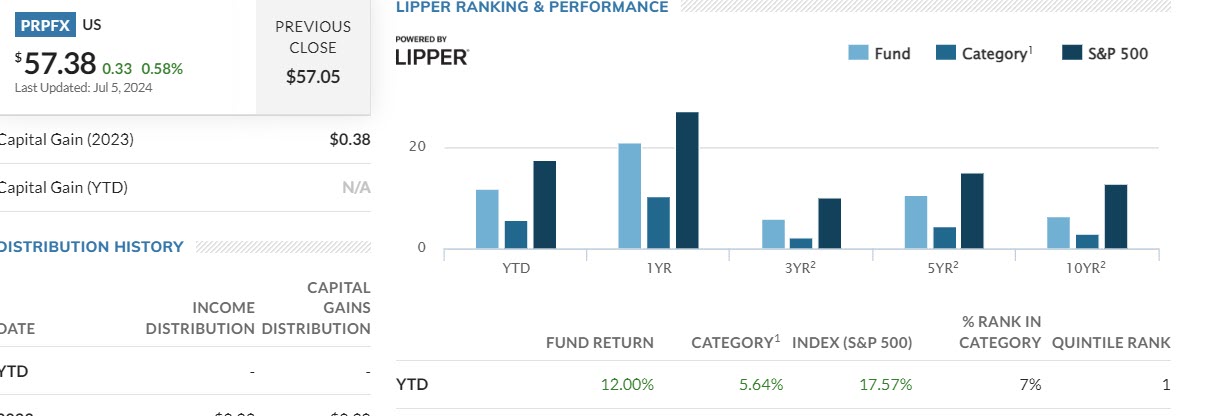

Not a bad idea...although first I would I would like to see what percent of the the underperformance of PRPFX vs the HBPP was due to the mutual fund's allocation vs the "classic" PP (i.e. 15% aggressive growth stocks, 15% natural resource stocks and REITs, 35% US Treasuries of varying maturities, 20% gold, 5% silver, and 10% in Swiss Franc bonds and bills vs the 4 x 25% PP) and how much of it was simply due to ridiculous fees (0.82% on the I class and 1.08% on the A class) and to Guggino thinking he could outsmart the market by active trading (he couldn't and didn't).

GestaltU had two posts comparing the PP with PRPFX ( "Permanent Portfolio Shakedown" Pts 1 and 2) which clearly showed the PP outperformed from 1983 to 2012 but it was essentially a wash after the high expense ratio of PRPFX was factored out. This means that in a potential rising rate environment the PP might actually underperform PRPFX's allocation given that PRPFX--being modestly biased to protecting against inflation rather than deflation--has generally kept mostly to ITTs and STTs rather than LTTs for its 35% Treasury sleeve (IIRC it was calculated here on this very forum that PRPFX could be blended 92/8 with EDV to create a portfolio with approximately the same bond duration as the 4 x 25 PP).

One thing is for sure; if you could charge maybe 15 or 20 basis points (with a credible promise to reduce to 10 basis points once AUM was large enough) for PRPFX's allocation in an ETF you would only have to poach about 11% or 12% of the current PRPFX's assets to break even; from Meb's podcasts in 2014 and 2018 he and his guest pinned the one-time first year cost for registrations, SEC filings, etc as around $150K to $250K and then ongoing costs of actually running the fund at $200K to $250K (so the first year's cost could be as much as $450K or $500K but after that it would be only the ongoing costs you would have to pay). PRPFX currently has assets (across all share classes) of $2.03 billion; even just 10% of that would more than cover the ongoing costs and would basically be at break-even for the first year's costs (which means that after the first year you could cut the fee to 15 basis points, then 14, then 13, etc as the asset base got larger). Now, if we could just get a list of PRPFX's shareholders......