If you’re familiar with the Permanent Portfolio strategy proposed by Harry Browne, you know the concept is elegant in its simplicity:

The economy moves through 4 macro scenarios:

The economy moves through 4 macro scenarios: Expansion

Expansion Recession

Recession Inflation

Inflation Deflation

DeflationSo, you diversify your assets equally:

25% Stocks (for growth)

25% Stocks (for growth)🏛 25% Bonds (for recession)

25% Gold (for inflation)

25% Gold (for inflation) 25% Cash (for deflation)

25% Cash (for deflation)The logic is sound — but here’s the real question:

Have these economic environments really happened 25% of the time each?

Have these economic environments really happened 25% of the time each? Not exactly. Historical data for the U.S. (since 1900) and Europe (mainly post-1950) tells a different story:

Not exactly. Historical data for the U.S. (since 1900) and Europe (mainly post-1950) tells a different story:⸻

Historical Occurrence of Each Scenario

Historical Occurrence of Each Scenario United States (NBER, CPI, FRED data):

United States (NBER, CPI, FRED data):•

Expansion (GDP growth, low inflation): ~65–70% of years•

Recession (GDP contraction): ~15%•

High Inflation (CPI > 5%): ~10–12%•

Deflation (CPI < 0%): ~3–5% Europe (post-WWII OECD/ECB data):

Europe (post-WWII OECD/ECB data):•

Expansion: ~60–65%•

Recession: ~20%•

Inflation: ~10–15%•

Deflation: Very rare — mostly post-2008 in some eurozone countries⸻

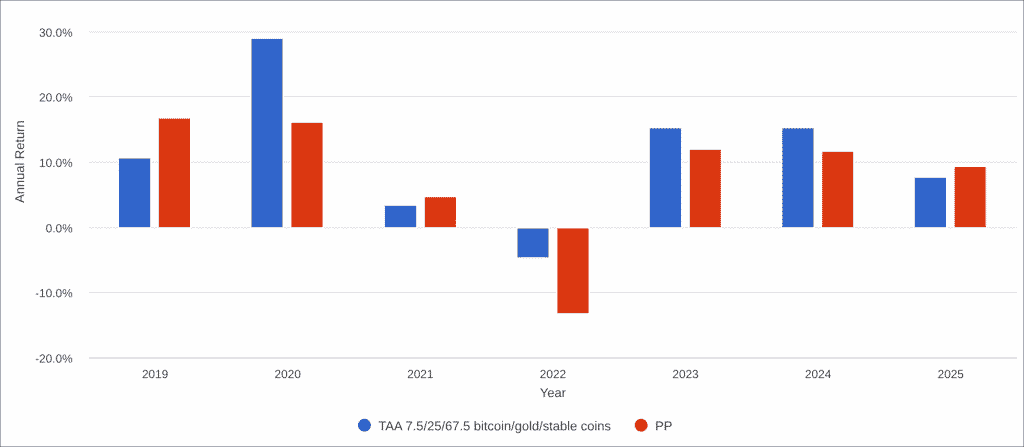

So… Is the 25/25/25/25 allocation realistic?

So… Is the 25/25/25/25 allocation realistic? From a hedging strategy, it works — because you’re always protected. But from a probability-weighted perspective, expansion dominates, and deflation is a rare outlier.

From a hedging strategy, it works — because you’re always protected. But from a probability-weighted perspective, expansion dominates, and deflation is a rare outlier.Still, Harry Browne’s genius was in building a “sleep-well-at-night” portfolio that doesn’t require prediction — just preparation.

⸻

Why This Still Matters

Why This Still Matters “Most of the time, economies grow. But when they don’t, you better be ready.”

“Most of the time, economies grow. But when they don’t, you better be ready.”⸻

Question for Permanent Portfolio followers:

Question for Permanent Portfolio followers:We know the classic split is 25% each — but based on modern macro data, what percentages do you actually use today?

Do you keep it pure, or do you tweak based on inflation risks, global instability, or regional factors?

Let’s hear your version.

we can reduce a little bit the cash

we can reduce a little bit the cash