Hey all, greetings! A rare post from me today....still way too busy to do much more than check in occasoinally to read posts, but I do have a topic for the group to ruminate on.

For the past decade, I've focused on building up cash reserves in my taxable investment account. Cash was ideal for taxable because it threw off almost no interest and of course had no gains. Whereas, I was preferring to load up my Roth IRA with stocks because of their growth potential.

Now the situation is reversed. Cash is burning a hole in my pocket and the tax treatment of interest sucks even if you stick with treasuries. I'm realizing that I should be parking "deep" cash, especially T bills, in the Roth IRA and getting individual stocks (not funds) for my taxable account. (Stock funds throw off a lot of capital gains and ordinary dividends, whereas with individual stocks, you aren't forced to take capital gains and every penny of the dividends are qualified.)

Is anyone else doing this, and is there a strategy involved? The Bogleheads wiki says you can effectively do this by swapping cash and stocks between taxable and Roth as needed, so you aren't actually taking money out of the Roth. There might be a snag with me though: I may need to loan large amounts of cash to my mother to fund her Alzheimer's care, as most of her assets are tied up in illiquid investments. So I can easily imagine a scenario in the next few years requiring me to sell a lot of stocks. (In the last 5 years of the standard Alzheimer's progression, costs are expected to run in the $250K-$300K/year range. If that sounds scary, then yes, be scared, because that's where a third of us are going to be eventually and there is no insurance vehicle in existence that will help.)

BTW it does help that I'm over age 59.5 and can draw from the Roth IRA directly if needed. With my current income though, I have limited ability to stoke the Roth for the foreseeable future.

Best place for cash

Moderator: Global Moderator

-

dualstow

- Executive Member

- Posts: 15791

- Joined: Wed Oct 27, 2010 10:18 am

- Location: foot of Mt Belzoni

- Contact:

Re: Best place for cash

Bump.

RIP Chuck Norris / I will be out of town in April and unable to respond to tickets. Sorry about that.

-

boglerdude

- Executive Member

- Posts: 1577

- Joined: Wed Aug 10, 2016 1:40 am

- Contact:

Re: Best place for cash

A total market fund doesnt sell. Vanguard sweep account 4.5%. That might be the "repo," it wasnt fair that only banks could have a savings account with the Fed

https://old.reddit.com/r/wallstreetbets ... time_ever/

edit1: HM Bradley 4.2% https://www.bogleheads.org/forum/viewtopic.php?t=348998

https://old.reddit.com/r/wallstreetbets ... time_ever/

edit1: HM Bradley 4.2% https://www.bogleheads.org/forum/viewtopic.php?t=348998

Re: Best place for cash

Sophie,sophie wrote: ↑Sun Feb 19, 2023 8:20 am I may need to loan large amounts of cash to my mother to fund her Alzheimer's care, as most of her assets are tied up in illiquid investments. So I can easily imagine a scenario in the next few years requiring me to sell a lot of stocks.

BTW it does help that I'm over age 59.5 and can draw from the Roth IRA directly if needed. With my current income though, I have limited ability to stoke the Roth for the foreseeable future.

You've written on here before about the situation with your mom but I just wanted to say that I'm sorry you and she are going through this. And this may be sacrilege to post here but I would put your question out to the Bogleheads community as well. There are lots of personal finance wizards & accountants over there. This forum is very quite at the moment as you can see from the lack of response to your post.

Anyway, it seems to me that you will want liquidity in your taxable account above all else, and I don't know of a better way to do that than holding nominal treasuries. And, yes, I read what you wrote about taxes but I don't think you want that fact to push you into riskier investments that you may have to sell at a loss to fund your mom's care.

I would hang onto that Roth money if at all possible as you can never really get it back once it's gone. I definitely have tried to beef up my Roth account in recent years but there's just no substitute for time & compounding.

Re: Best place for cash

Like you, I've been keeping a large proportion of cash allocation in taxable because, as you say, there were no tax consequences in recent years: (1) no real interest income to speak of, (2) if needed to withdraw for an emergency, no capital gains incurred to sell from a Money Market Fund. It's made sense for a while, but now is understandably at odds with Harry Browne's tax deferred priority order per radio show episode October 24, 2004:sophie wrote: ↑Sun Feb 19, 2023 8:20 am For the past decade, I've focused on building up cash reserves in my taxable investment account. Cash was ideal for taxable because it threw off almost no interest and of course had no gains. Whereas, I was preferring to load up my Roth IRA with stocks because of their growth potential.

Now the situation is reversed. Cash is burning a hole in my pocket and the tax treatment of interest sucks even if you stick with treasuries. I'm realizing that I should be parking "deep" cash, especially T bills, in the Roth IRA and getting individual stocks (not funds) for my taxable account. (Stock funds throw off a lot of capital gains and ordinary dividends, whereas with individual stocks, you aren't forced to take capital gains and every penny of the dividends are qualified.)

Is anyone else doing this, and is there a strategy involved?

1st cash

2nd bonds

3rd stocks

4th gold

I did move the last of my LTT to tax deferred in 2022, but was not focused on the cash segment. Now that T-Bills are paying over 4%, this has got me thinking too. I still have a fair amount of gold in tax deferred, so I may begin switching more gold/cash between IRA/taxable to reduce taxable interest income. But if I were to switch stocks/cash instead, I would not be comfortable selecting individual stocks. Like boglerdude mentions, VTI Total Market should not be generating a lot of capital gains. And the dividend yield is only 1.6%, so that's a third of the income that VUSXX MMF is now generating. Most of the VTI dividends should be qualified for better tax treatment. If I had to pick an individual stock? Maybe Berkshire Hathaway. It is kind of like a fund in the form of a stock. Ironically it does not pay a dividend (since 1967) even though it owns many dividend paying stocks.

Release the Epstein Files

-

boglerdude

- Executive Member

- Posts: 1577

- Joined: Wed Aug 10, 2016 1:40 am

- Contact:

Re: Best place for cash

iBond new rate 3.38%

Are all prices up 30% yet? Cuz thats how much they printed.

https://tipswatch.com/2023/04/12/march- ... e-at-3-38/

Are all prices up 30% yet? Cuz thats how much they printed.

https://tipswatch.com/2023/04/12/march- ... e-at-3-38/

Re: Best place for cash

Cash in a near 0% interest rate world was great, could be hard cash/currency with no counter-part risk. Stuffed under the mattress alongside gold. A reversion to positive interest rates times means that cash has to be deposited/invested elsewhere, back to older times of 'rate tarting' around. The prior accepted common activity of shifting cash around in the absence of having to do that raises awareness of how inconvenient that actually is. Other than regular rate-tarting and the associated trading activity that is inclined to induce (moving capital from within tax efficient/exempt to taxable if a better taxable rate can be secured, to only later having to reverse that around again), the Larry Portfolio concept struck a note with me, shifting bond (cash) risk over to the stock side, maybe holding a bit more stock weighting whilst leaving cash as hard-currency cash. Historically since 1972 T-Bills 4% nominal, Small Cap Value around three times that, so one third SCV, two thirds hard cash ... type concept.

Excepting if cash is earning perhaps 5% or more rates of return

Hard cash when rates are 0%

33/67 SCV/hard cash when rates are 2% to 4.99%

Treasury bills when rates are 5%+

Excepting if cash is earning perhaps 5% or more rates of return

Hard cash when rates are 0%

33/67 SCV/hard cash when rates are 2% to 4.99%

Treasury bills when rates are 5%+

Re: Best place for cash

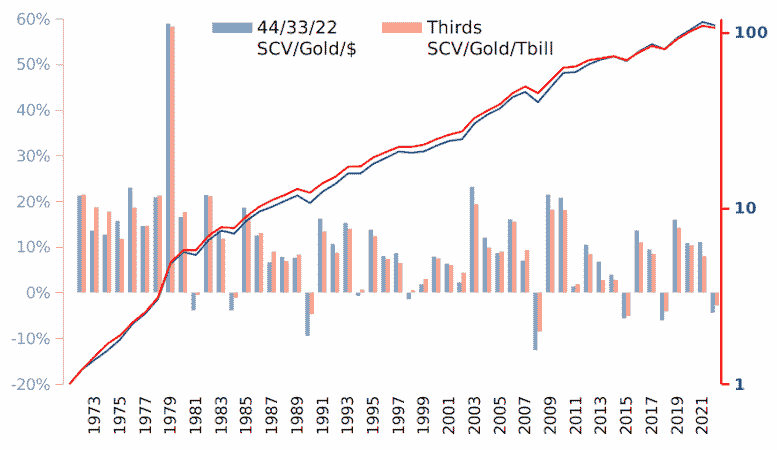

Asset allocation of thirds each SCV/Gold/T-Bills.

Swap the 'bond' (T-Bills) 'risk' over to the stock side, replace with 33/67 SCV/hard $ bills.

44.4 SCV/33.3 Gold/22.2 hard US$ bills compared to thirds each SCV/Gold/T-Bills (nominal) ...

and other than a bit more portfolio volatility, pretty much identical in overall reward/outcome (5.5% annualized real). Left Y-axis/bars = yearly total returns. Right Y-axis/lines = accumulation (log scale).

55% no counter-party risk (physical gold and hard US$ bills stuffed under the mattress)

Had expected that the high interest rates of the 1970's/1980's might have induced a wider deviation/drift, but apparently not.

Data sourced from Portfolio Visualizer (total returns 1972-2022 inclusive).

Swap the 'bond' (T-Bills) 'risk' over to the stock side, replace with 33/67 SCV/hard $ bills.

44.4 SCV/33.3 Gold/22.2 hard US$ bills compared to thirds each SCV/Gold/T-Bills (nominal) ...

and other than a bit more portfolio volatility, pretty much identical in overall reward/outcome (5.5% annualized real). Left Y-axis/bars = yearly total returns. Right Y-axis/lines = accumulation (log scale).

55% no counter-party risk (physical gold and hard US$ bills stuffed under the mattress)

Had expected that the high interest rates of the 1970's/1980's might have induced a wider deviation/drift, but apparently not.

Data sourced from Portfolio Visualizer (total returns 1972-2022 inclusive).