Page 1 of 1

Long Treasurys

Posted: Sun Feb 01, 2026 11:39 am

by foglifter

I’ve been revisiting the role of LTTs in my Golden Butterfly-ish portfolio and have really appreciated the depth of discussion here. Reading the recent “Safe Haven Status” thread prompted me to take another look at how I’m thinking about LTTs within this framework.

I understand the classic PP rationale: LTTs are held primarily as a deflation and recession hedge, not as a return engine. From that lens, 2022 looks less like a failure and more like an inflation/rate-shock regime where LTTs aren’t expected to shine. Still, it’s hard not to reflect on how that episode felt in practice and what it implies for correlations and drawdowns during inflationary periods.

My bond allocation is currently a STT/LTT barbell, consistent with PP/GB design. I’m thinking through whether, in real-world use, it still makes sense to:

a) keep the barbell as designed

b) substitute ITTs for LTTs

c) tilt more toward STTs and accept less convexity

For context, I hold some ~3%-yielding long-term Treasuries purchased in 2019 that are currently down -27%. I’m comfortable with duration risk conceptually, but I’m more interested in how LTTs actually function over long holding periods — particularly through full cycles of inflation, disinflation, and recession.

I’m not trying to forecast rates or inflation. I’m really just hoping to learn from folks who’ve actually lived with PP/GB allocations through multiple market cycles. How do you think about the role of LTTs today — in terms of diversification, rebalancing, and overall portfolio resilience over the long run?

Re: Long Treasurys

Posted: Sun Feb 01, 2026 3:58 pm

by Smith1776

My concern with long-term treasury bonds in the PP has always been that their volatility and risk profile are not constant. They're both higher when rates are lower, and lower when rates are higher.

Fortunately, I found a solution here in Canada. I'm sure similar solutions exist in the U.S.

I found a long-term treasury bond fund that targets a specific

duration rather than a specific

maturity.

https://www.td.com/ca/en/asset-manageme ... l-Bond-ETF

The ETF is TCLB, and it targets a 15-year duration regardless of the prevailing interest rate. When rates are low, it buys bonds on the shorter side. When rates are high, it buys bonds on the longer side.

This helps to ameliorate concerns about the asymmetric risk-reward trade-offs of long bonds when rates are low.

Re: Long Treasurys

Posted: Sun Feb 01, 2026 8:34 pm

by boglerdude

Most bond funds keep consistent duration, maybe there's another way to explain that fund

If you got burned holding LTTs at 2%, like I did, it's on you. Zero lower bound + shrinking population(and inflation to keep the lines going up), which Browne may not have considered.

Re: Long Treasurys

Posted: Mon Feb 02, 2026 10:37 am

by flyingpylon

I've been thinking about long-term bonds too, and the only things I know for sure are that I don't know very much and that I can't predict the future. So I don't claim to have any answers.

I think it depends on your time frame. I've never owned bonds (or even paid attention to them) during an extended down period so this is new to me. However, I questioned stocks (in retrospect) between 2000-2011, questioned gold from 2012-2020, and of course cash was "trash" for a long time too. I bought and held them all as part of the PP and then GB, and things have worked out pretty well overall, by design. I made some money by rebalancing out of bonds when they popped in 2020 but of course it's pretty much been downhill from there. Heck, I still have a small batch of 1.875% bonds that are down 45%! Part of me wants to get rid of them just so I don't have to look at them anymore, but another part of me wants to see if convexity is really a thing.

Sometimes when I question a particular asset I read this blog post from Tyler at Portfolio Charts:

How to Survive and Make Money in the Matrix

Also, "The Algorithm" sends things my way about potential disinflation/deflation that make me wonder where we're headed. Some people say that tariffs provide some protection against global deflation so perhaps the effects would be muted in the US. I don't claim to know either way.

Here's a post I saw recently from someone that calls himself "Common Sense Investor" titled

The Biggest Trade of 2026 Isn't Stocks - It's Bonds!

Maybe he's right, or maybe not. ¯\_(ツ)_/¯

Re: Long Treasurys

Posted: Mon Feb 02, 2026 2:46 pm

by mathjak107

his points are very strong

Re: Long Treasurys

Posted: Mon Feb 02, 2026 3:14 pm

by I Shrugged

Yes, the kicker is that we could experience short or longer term deflation, which would shake the world. Although, we (including me) all assume that they will create money to prevent that. Ultimately leading to persistent double digit inflation. Honestly I have found it more productive to not try to guess these things. I don't love treasuries but in the context of the portfolio they haven't killed me. In 2009 I switched a tax deferred account of ~$67 (leaving zeroes to the imagination) to VG Long Term Treasury Admiral Fund, and haven't touched it since. It's now at $104. I'm too lazy to figure out the IRR. It's not great but as I say, it didn't kill me. And that's with the rates we've seen.

Although I think it was up to 150 ish at one time. :/

Maybe rebalancing would have helped but that's not the point here. It's been a slog, but it was there to be called upon.

Re: Long Treasurys

Posted: Mon Feb 02, 2026 6:57 pm

by foglifter

flyingpylon, thanks for posting the links! The CSI's points seem reasonable.

Re: Long Treasurys

Posted: Tue Feb 03, 2026 4:26 am

by mathjak107

I Shrugged wrote: ↑Mon Feb 02, 2026 3:14 pm

Yes, the kicker is that we could experience short or longer term deflation, which would shake the world. Although, we (including me) all assume that they will create money to prevent that. Ultimately leading to persistent double digit inflation. Honestly I have found it more productive to not try to guess these things. I don't love treasuries but in the context of the portfolio they haven't killed me. In 2009 I switched a tax deferred account of ~$67 (leaving zeroes to the imagination) to VG Long Term Treasury Admiral Fund, and haven't touched it since. It's now at $104. I'm too lazy to figure out the IRR. It's not great but as I say, it didn't kill me. And that's with the rates we've seen.

Although I think it was up to 150 ish at one time. :/

Maybe rebalancing would have helped but that's not the point here. It's been a slog, but it was there to be called upon.

tracking inflation since 2009 puts it on par with inflation pretty much so zero real return but a negative real return after taxes eventually are paid

Re: Long Treasurys

Posted: Tue Feb 03, 2026 5:54 pm

by I Shrugged

mathjak107 wrote: ↑Tue Feb 03, 2026 4:26 am

I Shrugged wrote: ↑Mon Feb 02, 2026 3:14 pm

Yes, the kicker is that we could experience short or longer term deflation, which would shake the world. Although, we (including me) all assume that they will create money to prevent that. Ultimately leading to persistent double digit inflation. Honestly I have found it more productive to not try to guess these things. I don't love treasuries but in the context of the portfolio they haven't killed me. In 2009 I switched a tax deferred account of ~$67 (leaving zeroes to the imagination) to VG Long Term Treasury Admiral Fund, and haven't touched it since. It's now at $104. I'm too lazy to figure out the IRR. It's not great but as I say, it didn't kill me. And that's with the rates we've seen.

Although I think it was up to 150 ish at one time. :/

Maybe rebalancing would have helped but that's not the point here. It's been a slog, but it was there to be called upon.

tracking inflation since 2009 puts it on par with inflation pretty much so zero real return but a negative real return after taxes eventually are paid

Yes. In my case I am going to direct the RMDs to charity which will eliminate the taxes.

Re: Long Treasurys

Posted: Wed Mar 04, 2026 2:32 pm

by ppnewbie

I just added to my allocation of long bonds I buy the actual bonds themselves at a full 30 years. If we dont default and / or inflate away our country, this is still an assymetric deflation hedge IMHO. I was actually tempted to buy EDV which even more volatile.

Re: Long Treasurys

Posted: Sat Mar 07, 2026 6:50 am

by whatchamacallit

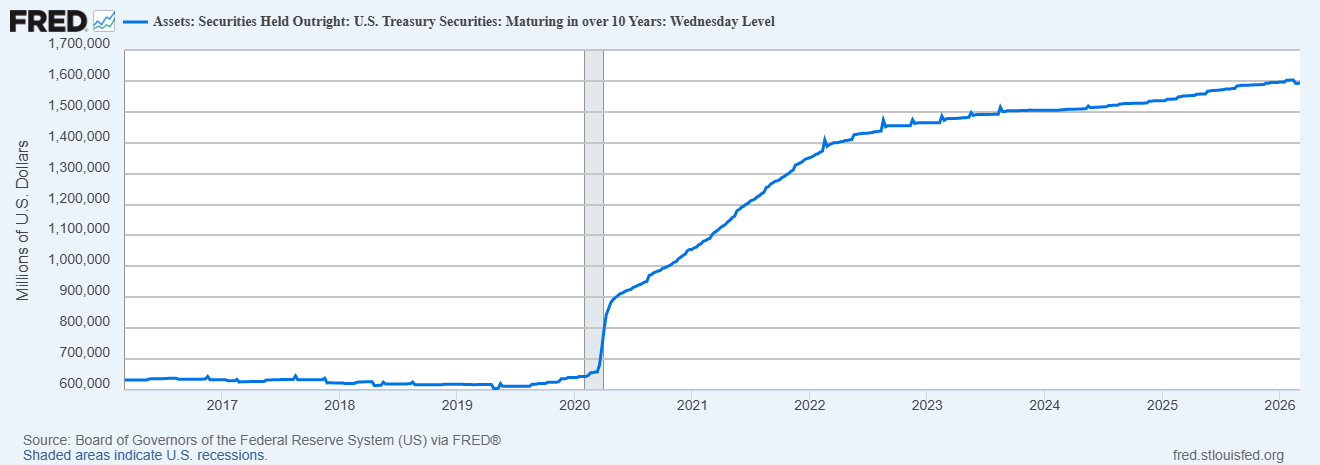

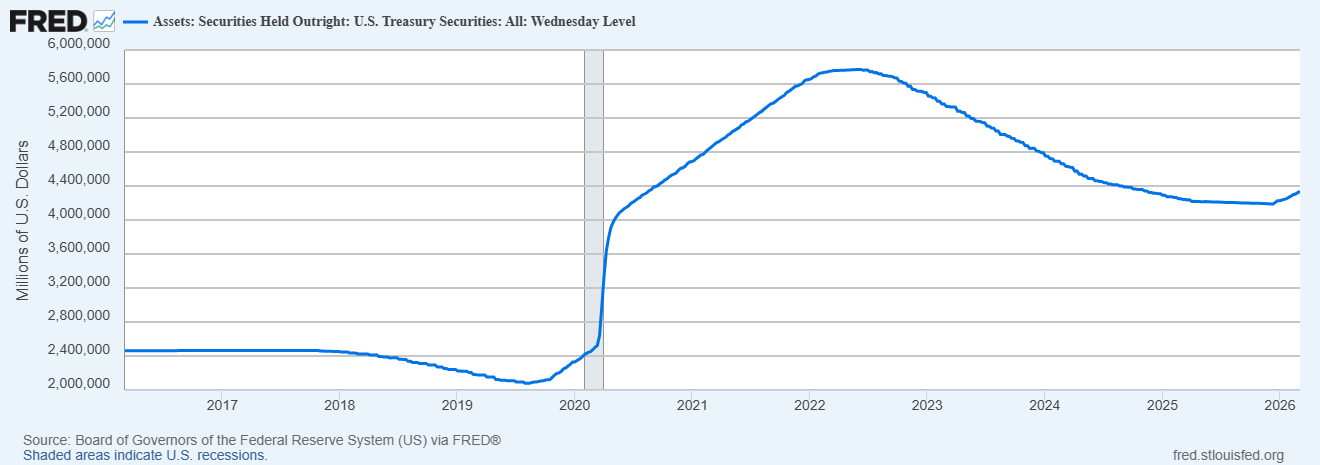

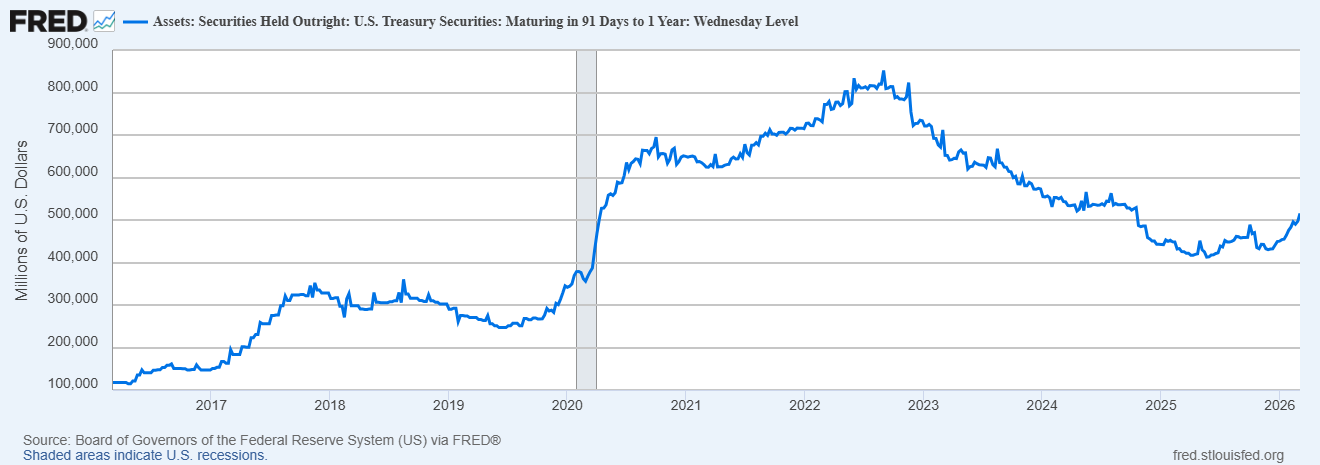

I don't like them still. There is not enough of a spread to make them worth it for me. I do also think the long duration bond rates are being suppressed by the Federal Reserve.

Look at the long duration holdings by the federal reserve vs the short duration or total holdings:

https://fred.stlouisfed.org/series/TREAS10Y

- fredgraph.png (65.22 KiB) Viewed 4508 times

https://fred.stlouisfed.org/series/TREAST#

- fredgraph (1).png (65.54 KiB) Viewed 4508 times

https://fred.stlouisfed.org/series/TREAS911Y

- fredgraph (2).png (75.58 KiB) Viewed 4508 times

Re: Long Treasurys

Posted: Sat Mar 07, 2026 7:36 am

by mathjak107

they have been holding up well considering 90 dollar a barrel oil .

but being so long in duration they are looking out well past this mess.

we have had almost every recession when oil prices were high .

there are one or two exceptions i think

Re: Long Treasurys

Posted: Sat Mar 14, 2026 5:31 am

by mathjak107

backed up the truck yesterday and loaded up on VGLT and GOVT at these rates .

they are substantially above short term rates now by a wide margin .

i don’t ever expect to catch the top and nav prices will fall more from here most likely but eventually this war will end and while we may see higher inflation i still think these rates will be fine , especially if the typical oil shock recession follows .

also loaded up the gold position yesterday as that too fell substantially from the highs a few weeks ago .

this is one of those times anything can happen including a repeat of 2022 when risk was off in all assets but longer term things have a way of settling down and resuming . we just don’t know when

Key Historical Oil Shock Recessions

1973–1975 Recession: Following the Arab-Israeli War, OAPEC imposed an embargo, causing oil prices to nearly quadruple and triggering a severe global downturn.

1979–1980 Energy Crisis: The Iranian Revolution sparked a massive supply disruption, with oil prices doubling, causing a global recession.

1990–1991 Recession: Triggered by the Gulf War and subsequent oil price spikes.

2007–2008 Financial Crisis: Oil prices reached an all-time high of $145 a barrel in July 2008, contributing to the severity of the global recession

Re: Long Treasurys

Posted: Sat Mar 14, 2026 10:44 pm

by boglerdude

If the Fed stops curve-control we're cooked. And why should they buy long? Government could run on perpetual 1-year buys (MMT).

https://old.reddit.com/r/EconomyCharts/ ... w_alltime/

Re: Long Treasurys

Posted: Sun Mar 15, 2026 12:36 pm

by amdda01

mathjak107 wrote: ↑Sat Mar 14, 2026 5:31 am

backed up the truck yesterday and loaded up on VGLT and GOVT at these rates .

they are substantially above short term rates now by a wide margin .

i don’t ever expect to catch the top and nav prices will fall more from here most likely but eventually this war will end and while we may see higher inflation i still think these rates will be fine , especially if the typical oil shock recession follows .

also loaded up the gold position yesterday as that too fell substantially from the highs a few weeks ago .

this is one of those times anything can happen including a repeat of 2022 when risk was off in all assets but longer term things have a way of settling down and resuming . we just don’t know when

Key Historical Oil Shock Recessions

1973–1975 Recession: Following the Arab-Israeli War, OAPEC imposed an embargo, causing oil prices to nearly quadruple and triggering a severe global downturn.

1979–1980 Energy Crisis: The Iranian Revolution sparked a massive supply disruption, with oil prices doubling, causing a global recession.

1990–1991 Recession: Triggered by the Gulf War and subsequent oil price spikes.

2007–2008 Financial Crisis: Oil prices reached an all-time high of $145 a barrel in July 2008, contributing to the severity of the global recession

MJ,

How come no TLT? And what was your breakdown of VGLT vs GOVT?

Re: Long Treasurys

Posted: Sun Mar 15, 2026 3:08 pm

by mathjak107

vglt seems a tad less volatile .

60% vglt and 40% govt make up the bond portion

Re: Long Treasurys

Posted: Sun Mar 15, 2026 3:14 pm

by flyingpylon

mathjak107 wrote: ↑Sat Mar 14, 2026 5:31 am

backed up the truck yesterday and loaded up on VGLT and GOVT at these rates .

Wait, what? Is this a sign of the apocalypse?

Re: Long Treasurys

Posted: Sun Mar 15, 2026 3:22 pm

by mathjak107

finally some decent rates at a time there is a decent chance we could end up in another oil shock recession.

big difference from 1.6% rates when i warned to stay away from them

Re: Long Treasurys

Posted: Sun Mar 15, 2026 4:16 pm

by rtgyroscopic

mathjak107 wrote: ↑Sun Mar 15, 2026 3:22 pm

finally some decent rates at a time there is a decent chance we could end up in another oil shock recession.

big difference from 1.6% rates when i warned to stay away from them

Curious how big your truck was.. Are you closing in on a 25% chunk of bonds?

Re: Long Treasurys

Posted: Sun Mar 15, 2026 5:22 pm

by mathjak107

big enough to hold just under 7 figures worth.

about a 20% bond position