craigr wrote:

Why should cycles be present in the markets? The periods you point out in your example all have rational economic explanations for them.

Cycles are present because of the high probability of humans repeating the same or similar actions towards capital allocation and misallocation. Sure, the periods all have rational explanations, but does that invalidate the thesis or suggest that eventually fundamentals always win one way or the other?

The 1970s were a period after the gold standard broke. Inflation raged. It wasn't a cycle.

Why did the gold standard break? Because gold was increasingly worth more on the open market in London than at the gold window in Washington. Countries were draining U.S. reserves so either the U.S. went broke or the U.S. devalued. Maximum optimism in equities ended in 1966 which began a period of rising pessimism for the dollar's value vis a vis gold. The U.S. allowed the dollar to devalue vs gold through the 70s which ended with maximum pessimism in January 1980.

Then in the early 1980s the Fed finally got serious and stopped the chaos through some serious rate tightening. Again, this was not a cycle.

But why in the early 80s? Random occurrence or as a result of rapidly escalating inflation at over 14% to start the decade? I say the latter. And what did Volker's interest rates do to equities? It crushed them along with the inflation. The tight money recession led to incredibly attractive valuations for equities in 1982, which provided a driver for increased investment again.

Periods before were pockmarked with world events like wars, depressions, etc.

Haven't wars typically been started because of economic upheaval? Aren't depressions started because valuations have become so high that eventually the market realizes its mistake en masse? The main point I am making is that people collectively go through a routine cycle that runs something like:

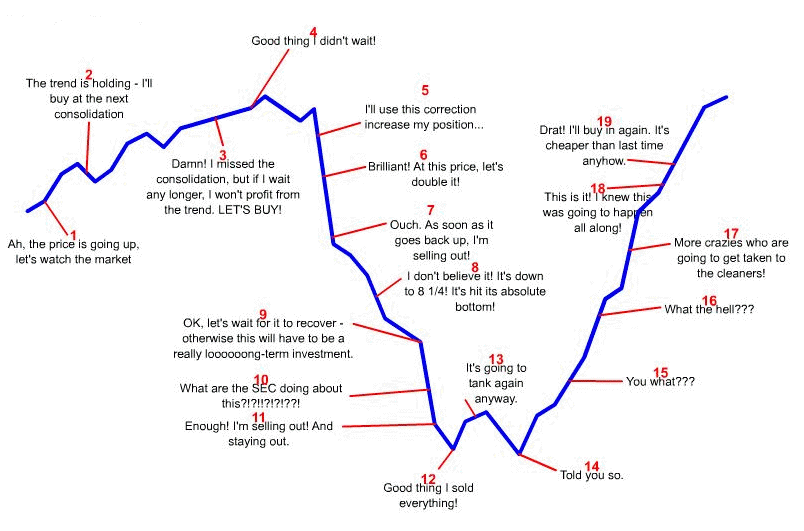

Ultra low optimism in paper: fantastic valuations, little investor participation

Low optimism in paper: good valuations, some investor participation

Undecided: fair valuations, even bulls/bears

High optimism in paper: expensive valuations, lots of investor participation

Highest optimism in paper: stratospheric valuations, nearly all investor participation

It's the same cycle in reverse for hard assets. When bubbles pop in paper assets, investors will increasingly run to the safest of all forms of money: gold. When pessimism becomes so great in paper assets, the maximum amount of investors will have their value in money/gold. Since this is not productive (gold is a shiny rock, remember), investors will again start to invest in paper once the coast is clear.

Things become more cloudy in a fiat system. When bubbles pop, you have two choices: crash or devalue. It's more politically palatable to devalue the currency to support asset values. The 30s and 70s give us great case studies in the two sides of the spectrum. In 1933, gold was money. Stocks crashed to gold because nominal was real value. Stocks didn't create another liftoff event until 1947--after the war was over and the U.S. had massive inflows of gold which it could leverage the money supply on. In 1966, investors turned to gold again in international markets, forcing the U.S. to devalue in real terms. Stocks crashed again in real terms even though the nominal values stayed elevated.

Even if there was a gold cycle, why would it matter to Americans that could not own gold between 1933-1974 and was price controlled? And before 1933 there was not a gold cycle in the US because it was all price controlled also and was legal money anyway.

It would matter to Americans from a stocks standpoint. Harry Browne knew this. Sure, he said "awe, shucks, I got lucky" because he wasn't the type to say "yeah, I told you so!" He also didn't want the average investor with little monetary knowledge to get sucked into speculating on such things like he did because he had the knowledge that the average investor doesn't. It's safer for the public to tell the public that he got lucky. I admire his modesty, but I'm afraid that's all it is.

Prior to the Fed in 1913, the boom/bust cycle was still there--but both the booms and the busts weren't as large until after the Fed's existence.

Markets are made of people and people don't learn from history very often--they repeat the exact same mistakes or similar mistakes. They also act collectively most of the time. They routinely see what other people are doing for social proof. They act the same way and they think the same way based on how other people think. No one wants to admit it but its part of human nature. This all feeds into the existence of cycles. If people acted like robots--sure, there wouldn't be cycles.

But seriously, I can't say for certain when the low will be for equities and the high for gold. What I do believe is that at some point in the next 10 years or less, we will find that low point in real terms. Whether we get there via inflation/deflation/stagflation it really doesn't matter. Those are decisions for other people not named Wonk. We will need maximum pessimism in financial assets to get there and we will need maximum optimism in gold to get there. Traditionally, that metric has been gold value in fiat currency = monetary base of the same currency at a minimum from the hard assets side. The metric for U.S. stocks has been PE10 at 10 or below.