I've been wondering: What if Long Term Treasuries start paying negative nominal interest rates? I believe that since Harry Browne developed the Permanent Portfolio, there has never been a time when the US long term Treasuries paid nominal interest rates that were negative.

But such negative rates would mean an outlay of cash to pay for the privilege of owning the bonds, with no guarantee of an increase in the market value of the bonds.

Has this question ever come up before? I did a search here, but could not find anything.

What about negative rates on LTTs?

Moderator: Global Moderator

-

murphy_p_t

- Executive Member

- Posts: 1675

- Joined: Fri Jul 02, 2010 3:44 pm

Re: What about negative rates on LTTs?

see http://gyroscopicinvesting.com/forum/ht ... ic.php?t=3 for closely related topic

Re: What about negative rates on LTTs?

I don't think that the yield curve would ever get that flat.

In fact, once people began seriously anticipating such a scenario it would probably be time to sell long term treasuries (not in the PP, of course, but as a speculative play).

In fact, once people began seriously anticipating such a scenario it would probably be time to sell long term treasuries (not in the PP, of course, but as a speculative play).

Q: “Do you have funny shaped balloons?”

A: “Not unless round is funny.”

A: “Not unless round is funny.”

Re: What about negative rates on LTTs?

Didn't we see negative real rates on LTT during the late 70's early 80's? This is actually a very strange time period that I cannot wrap my mind around. Why weren't LTT slaughtered? They seemed to escape without much pain (held their nominal value), even when interest rates were being dramatically increased. Would it have something to do with the environment of generally increasing rates since the 1950's, and was therefore anticipated?

I found this chart of the 10 year bonds rate, and here is one for the 30 year.

Code: Select all

Year TSM ST LT Gold Returns

1972 16.9 3.9 5.7 48.9 18.8

1973 -18.1 6.1 -1.1 75.6 15.6

1974 -27.2 9.1 4.4 70.5 14.2

1975 38.7 7.9 9.2 -22.7 8.3

1976 26.7 8.9 16.8 -3.8 12.2

1977 -4.2 3.7 -0.7 23.5 5.6

1978 7.5 5.5 -1.2 36.7 12.1

1979 23.0 10.4 -1.2 136.3 42.1

1980 32.7 14.1 -4.0 10.8 13.4

1981 -3.7 18.9 1.9 -32.8 -3.9

1982 20.8 19.5 40.4 12.5 23.3

1983 22.0 8.6 0.7 -14.3 4.2

1984 4.5 12.8 15.5 -20.2 3.2

1985 32.2 13.2 31.0 6.9 20.8

1986 16.1 11.9 24.5 22.9 18.8

http://crawlingroad.com/blog/2008/12/22/permanent-portfolio-historical-returns/

-

WildAboutHarry

- Executive Member

- Posts: 1090

- Joined: Wed May 04, 2011 9:35 am

Re: What about negative rates on LTTs?

If you were holding the 2007 Treasury Bond in 1977 at about 8% (according to the chart you listed), what do you suppose the price of that bond was in late 1980/early 1981?Gosso wrote:Why weren't LTT slaughtered?

This http://futures.tradingcharts.com/histor ... nuous.html shows them in the mid 60s in February 1980. Obviously your 30-year in 1977 would have been a 27-year in 1980, but that is quite a haircut.

Last edited by WildAboutHarry on Tue Apr 10, 2012 10:24 am, edited 1 time in total.

It is the settled policy of America, that as peace is better than war, war is better than tribute. The United States, while they wish for war with no nation, will buy peace with none" James Madison

Re: What about negative rates on LTTs?

With inflation running at an average rate of 8% or so during that period (1977-1981), it looks like bonds would have seen an annual inflation-adjusted loss of 10% or so in each year of that period.WildAboutHarry wrote:If you were holding the 2007 Treasury Bond in 1977 at about 8% (according to the chart you listed), what do you suppose the price of that bond was in late 1980/early 1981?Gosso wrote:Why weren't LTT slaughtered?

I don't know if that qualifies as getting slaughtered, but it's pretty bad.

Q: “Do you have funny shaped balloons?”

A: “Not unless round is funny.”

A: “Not unless round is funny.”

Re: What about negative rates on LTTs?

I found this neat tool that calculates the price/yield based on the changing price/yield. http://www.smartmoney.com/calculator/bo ... 988621833/WildAboutHarry wrote:If you were holding the 2007 Treasury Bond in 1977 at about 8% (according to the chart you listed), what do you suppose the price of that bond was in late 1980/early 1981?Gosso wrote:Why weren't LTT slaughtered?

So if the LTT went from a yield of 8% to 14% that would represent a 43% decline ($100 face value down to $57). If we spread this out over four years, and then factor in the average 10% interest payments, then it works out to a wash in nominal terms. But yes inflation does the most damage.

In our current situation with LTT around the 3% mark, then a jump in yield to 5.25% (same percent change as in late 70's of 75%) would look more painful in nominal terms, but inflation would not be quite as high.

Last edited by Gosso on Tue Apr 10, 2012 12:50 pm, edited 1 time in total.

Re: What about negative rates on LTTs?

I guess you would hope that your gold holdings would more than make up for your real loss on LTT's.

Re: What about negative rates on LTTs?

If EE bonds are still around and paying out a compounded 3.5% over 20 years, I'm just going to start up LLC after LLC until I drop all my negative interest LTT's.

"Men did not make the earth. It is the value of the improvements only, and not the earth itself, that is individual property. Every proprietor owes to the community a ground rent for the land which he holds."

- Thomas Paine

- Thomas Paine

Re: What about negative rates on LTTs?

Clive,

That makes sense. For some reason I hadn't fully factored in the interest payments in my previous thinking. I always envisioned that if interest rates doubled then I'd see a nominal loss of 50% on my long bonds. But if this process is drawn out over a few years then interest payments will take some bite out of that loss (for example, a 5% yield over four years is 20%, and would therefore see an average annual loss of 30%/4 = 7.5% for the long bonds). It will still hurt, but may not look as bad as I previously thought.

http://www.marketoracle.co.uk/Article34033.html

That makes sense. For some reason I hadn't fully factored in the interest payments in my previous thinking. I always envisioned that if interest rates doubled then I'd see a nominal loss of 50% on my long bonds. But if this process is drawn out over a few years then interest payments will take some bite out of that loss (for example, a 5% yield over four years is 20%, and would therefore see an average annual loss of 30%/4 = 7.5% for the long bonds). It will still hurt, but may not look as bad as I previously thought.

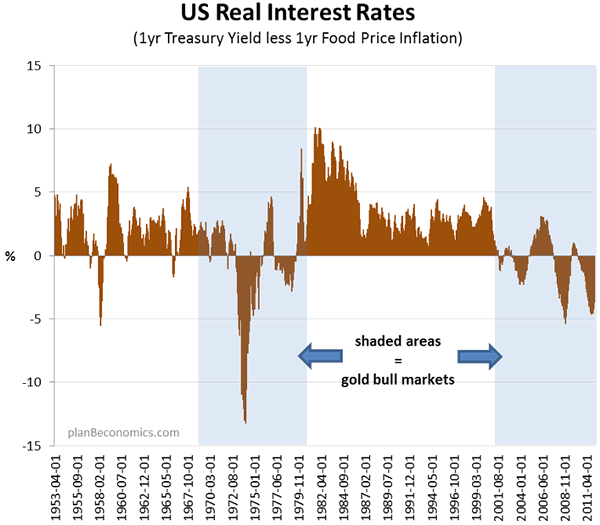

Probably, here is an interesting chart using one year treasuries:clacy wrote: I guess you would hope that your gold holdings would more than make up for your real loss on LTT's.

http://www.marketoracle.co.uk/Article34033.html

-

WildAboutHarry

- Executive Member

- Posts: 1090

- Joined: Wed May 04, 2011 9:35 am

Re: What about negative rates on LTTs?

That reminds me of the old (OK, very old) joke about Amazon.com. They lose money on every transaction, but they make up for it with volumeClive wrote: That doesn't make LTT's more riskier at lower yields than at higher yields however as in nominal terms you lose more, but in real terms you lose less.

It is the settled policy of America, that as peace is better than war, war is better than tribute. The United States, while they wish for war with no nation, will buy peace with none" James Madison

Re: What about negative rates on LTTs?

Since the Treasury is the creditor, any negative rates would really be a poorly disguised Wealth Tax lacking congressional authority.

Last edited by atrchi on Wed Apr 11, 2012 6:01 pm, edited 1 time in total.

Re: What about negative rates on LTTs?

I would still hold onto them. If they can drop to -1% then they can drop to -2% and continue to make capital gains.smurff wrote: I've been wondering: What if Long Term Treasuries start paying negative nominal interest rates?

I doubt this will ever happen, though.

"All men's miseries derive from not being able to sit in a quiet room alone."

Pascal

Pascal

Re: What about negative rates on LTTs?

Yes, this topic comes up from time to time on this forum. We had a good discussion on it several months ago:smurff wrote: I've been wondering: What if Long Term Treasuries start paying negative nominal interest rates?

[...]

Has this question ever come up before? I did a search here, but could not find anything.

http://gyroscopicinvesting.com/forum/ht ... ic.php?t=2

In discussing the idea of negative LTT rates, I think it's important to acknowledge not just that it's possible to drop from -1% to -2%, or from -2% to -3%, but also that the relative probability of each subsequent drop becomes smaller. So when LTT rates drop low enough (perhaps even negative), what we're really talking about is limited upside and virtually unlimited downside.AdamA wrote: If [LTTs] can drop to -1% then they can drop to -2% and continue to make capital gains.

I doubt this will ever happen, though.

In that other thread I mentioned above, I likened this to a casino bet in which the croupier offers to toss a coin and announces, "Heads it's a draw, tails you lose."

That's an exaggeration, of course, but the bet would still be something like: A small probability you'll enjoy a small net gain, and a large probability you'll suffer a large loss. It's like the inverse of a lottery ticket.

This question of what to do with LTTs in the PermPort as rates approach zero or even go negative has never been answered to my satisfaction. And that's okay, because some things in life don't have neat, tidy answers. On the one hand, it's true that it's possible for LTT rates to keep on going negative... down, down, down, without end. But we all know the probability of further rate declines decreases along with the rates themselves.

Ultimately, the point at which one thinks the downside potential starts to prohibitively outweigh the upside potential is a subjective one; there's no right answer. Personally, I will probably start converting some of my PermPort's LTTs into T-bills if LTT rates drop below about 1%.

Re: What about negative rates on LTTs?

If T-bill rates were even more negative would you still do this or would you perhaps go for an alternate arrangement? It seems that physical cash would beat them both.Tortoise wrote: Ultimately, the point at which one thinks the downside potential starts to prohibitively outweigh the upside potential is a subjective one; there's no right answer. Personally, I will probably start converting some of my PermPort's LTTs into T-bills if LTT rates drop below about 1%.

In such a weird world, I wonder whether I'd wind up drifting into an arrangement of something like 33% stocks and then 33% gold / 33% physical cash in a very, very safe place (or series of very, very safe places.)

Re: What about negative rates on LTTs?

I think we are getting closer to a "cashless" society. Canada is in the process of eliminating the penny, and is also researching a new method to digitally pay for small transactions...it would be called the MintChip, here is an article on it:Lone Wolf wrote:If T-bill rates were even more negative would you still do this or would you perhaps go for an alternate arrangement? It seems that physical cash would beat them both.Tortoise wrote: Ultimately, the point at which one thinks the downside potential starts to prohibitively outweigh the upside potential is a subjective one; there's no right answer. Personally, I will probably start converting some of my PermPort's LTTs into T-bills if LTT rates drop below about 1%.

In such a weird world, I wonder whether I'd wind up drifting into an arrangement of something like 33% stocks and then 33% gold / 33% physical cash in a very, very safe place (or series of very, very safe places.)

Here is another good article on it: http://www.theglobeandmail.com/news/tec ... le2399500/...

MintChip stores value in a physical chip, and transfers money between chips using heavily encrypted "value messages." The system has no cen-tralized database. "They're calling it anonymous ... their intention is that it's no more associated with who you are than [traditional] currency," said Jacqueline Chilton with Glenbrook Partners, a California-based payment consultant.

...

MintChip can handle any amount of money, but the Mint envisions it as a way to digitize small transactions, like bus fare, a song download or a stick of gum.

In a world without physical cash I can envision negative nominal interest rates on T-Bills, and possibly LLT. This would act as an incentive to spend the money, rather than save it, or at least that would be the hope. Of course the problem is that commodity prices would likely go crazy.

Re: What about negative rates on LTTs?

Thanks! I've long heard of these ideas but didn't realize that Canada was actually getting serious about testing the waters.Gosso wrote: In a world without physical cash I can envision negative nominal interest rates on T-Bills, and possibly LLT. This would act as an incentive to spend the money, rather than save it, or at least that would be the hope. Of course the problem is that commodity prices would likely go crazy.

Now to perform this interest rate magic, wouldn't MintChip have to go a step further and actively reduce the cash balance on a card over time, giving you an effective "negative yield"? (Gah, this reminds of that annoying "deterioration" behavior you have on some gift cards.)

If MintChip doesn't reduce the amount of "cash" on your chip, isn't it then still equivalent to mattress-stuffing? (And thus better than negative LTTs and really, really negative T-bills?) It seems like MintChip's goal is to really act like cash.

I imagine that if a "feature" to have your cash balance erode over time were included in MintChip, its adoption rate would not be very high.

Re: What about negative rates on LTTs?

Hmmm, but if paper bills and coins are eliminated, then you will have no choice but to use the MintChip as the new form of "cash" (unless a black-market for gold and silver coins develops). If a negative nominal interest rate is set, then your savings and the MintChip would both need to be depreciating at the negative interest rate. There is nowhere to hide your savings, except for in stocks, commodities, and fancy cars.Lone Wolf wrote:Thanks! I've long heard of these ideas but didn't realize that Canada was actually getting serious about testing the waters.Gosso wrote: In a world without physical cash I can envision negative nominal interest rates on T-Bills, and possibly LLT. This would act as an incentive to spend the money, rather than save it, or at least that would be the hope. Of course the problem is that commodity prices would likely go crazy.

Now to perform this interest rate magic, wouldn't MintChip have to go a step further and actively reduce the cash balance on a card over time, giving you an effective "negative yield"? (Gah, this reminds of that annoying "deterioration" behavior you have on some gift cards.)

If MintChip doesn't reduce the amount of "cash" on your chip, isn't it then still equivalent to mattress-stuffing? (And thus better than negative LTTs and really, really negative T-bills?) It seems like MintChip's goal is to really act like cash.

I imagine that if a "feature" to have your cash balance erode over time were included in MintChip, its adoption rate would not be very high.

Isn't this what the Central Banks want?

Also, I'm not saying this will happen, but could become a possibility if the Central Bankers become desperate and physical cash is eliminated. And if it does happen, then I'd be quite happy to own LLT at an interest rate of 0-1%, while the nominal interest rate is at -3%.

Here is an interesting quote from Wikipedia on negative nominal interest rates:

If they are already thinking about it in respect to our paper money, imagine how easy it would be for digital money.It has been proposed that a negative interest rate can in principle be levied on existing paper currency via a serial number lottery: choosing a random number 0 to 9 and declaring that bills whose serial number end in that digit are worthless would yield a negative 10% interest rate, for instance (choosing the last two digits would allow a negative 1% interest rate, and so forth). This was proposed by an anonymous student of N. Gregory Mankiw,[14] though more as a thought experiment than a genuine proposal.[16]

Re: What about negative rates on LTTs?

Right! But from what I read about the current MintChip system is that such "nominal depreciation" is not a feature that it could offer under the current architecture. I agree that it removes many barriers for MintChip v2.0 though!Gosso wrote: Hmmm, but if paper bills and coins are eliminated, then you will have no choice but to use the MintChip as the new form of "cash" (unless a black-market for gold and silver coins develops). If a negative nominal interest rate is set, then your savings and the MintChip would both need to be depreciating at the negative interest rate. There is nowhere to hide your savings, except for in stocks, commodities, and fancy cars.

I wonder whether people would stand for a cash replacement that had such an "auto-depreciation" back door. I know that a design feature like that would kick up an intense political firestorm in the US.

Yeah, that was an amusing idea. I've linked that before myself actually. Fortunately it's usually reassuringly called a "joke" and a "though experiment". Just one of those "jokes" that makes my stomach tie itself into dozens of teeny tiny little knots.Gosso wrote:Here is an interesting quote from Wikipedia on negative nominal interest rates:

Re: What about negative rates on LTTs?

I agree. It would be extremely upsetting for the population to actually see their savings shrink -- this is probably the largest hurdle to overcome with regards to negative nominal interest rates.Lone Wolf wrote: I wonder whether people would stand for a cash replacement that had such an "auto-depreciation" back door. I know that a design feature like that would kick up an intense political firestorm in the US.

I thought I'd throw it in as a "you never know".Lone Wolf wrote: Yeah, that was an amusing idea. I've linked that before myself actually. Fortunately it's usually reassuringly called a "joke" and a "though experiment". Just one of those "jokes" that makes my stomach tie itself into dozens of teeny tiny little knots.

Re: What about negative rates on LTTs?

I almost think the psychological affect of negative interest rates might launch gold to unreasonable highs. I'd like to see it happen more out of curiosity than anything.... at least maybe on the short-end.

"Men did not make the earth. It is the value of the improvements only, and not the earth itself, that is individual property. Every proprietor owes to the community a ground rent for the land which he holds."

- Thomas Paine

- Thomas Paine

Re: What about negative rates on LTTs?

Negative T-bill rates would most likely occur in a deflationary environment, so I probably wouldn't mind negative nominal T-bill rates all that much. Real T-bill rates would probably be less negative or even slightly positive, I imagine.Lone Wolf wrote:If T-bill rates were even more negative would you still do this or would you perhaps go for an alternate arrangement? It seems that physical cash would beat them both.Tortoise wrote: Ultimately, the point at which one thinks the downside potential starts to prohibitively outweigh the upside potential is a subjective one; there's no right answer. Personally, I will probably start converting some of my PermPort's LTTs into T-bills if LTT rates drop below about 1%.

In such a weird world, I wonder whether I'd wind up drifting into an arrangement of something like 33% stocks and then 33% gold / 33% physical cash in a very, very safe place (or series of very, very safe places.)

But yes, physical cash would be an even better option for those with the patience and desire to figure out safe yet convenient ways of storing it. Not sure I would be one of those people.

Last edited by Tortoise on Fri Apr 13, 2012 3:59 am, edited 1 time in total.

Re: What about negative rates on LTTs?

How about an inverted yield curve where short term treasuries are at 0% nominal, while long term treasuries have a -2 or -3% nominal rates. I could see this happening since no one is really interested in the interest payments from LTT. I think most "smart" investors buy LTT because they want the price movement. Who cares if the underlying value is being slightly eroded by -2% when you can potentially gain 30-50% from capital appreciation.

I'm not sure how this would work from a logistics point of view. I guess they would act the same as zeros, except the negative annual phantom interest is subtracted from the bond value.

I cannot think of an example of this ever occurring. Is there something fundamental that I'm missing on why this couldn't happen? Cash is still cash, LTT are still volatile instruments...

I'm not sure how this would work from a logistics point of view. I guess they would act the same as zeros, except the negative annual phantom interest is subtracted from the bond value.

I cannot think of an example of this ever occurring. Is there something fundamental that I'm missing on why this couldn't happen? Cash is still cash, LTT are still volatile instruments...

Last edited by Gosso on Tue Jul 24, 2012 8:52 pm, edited 1 time in total.