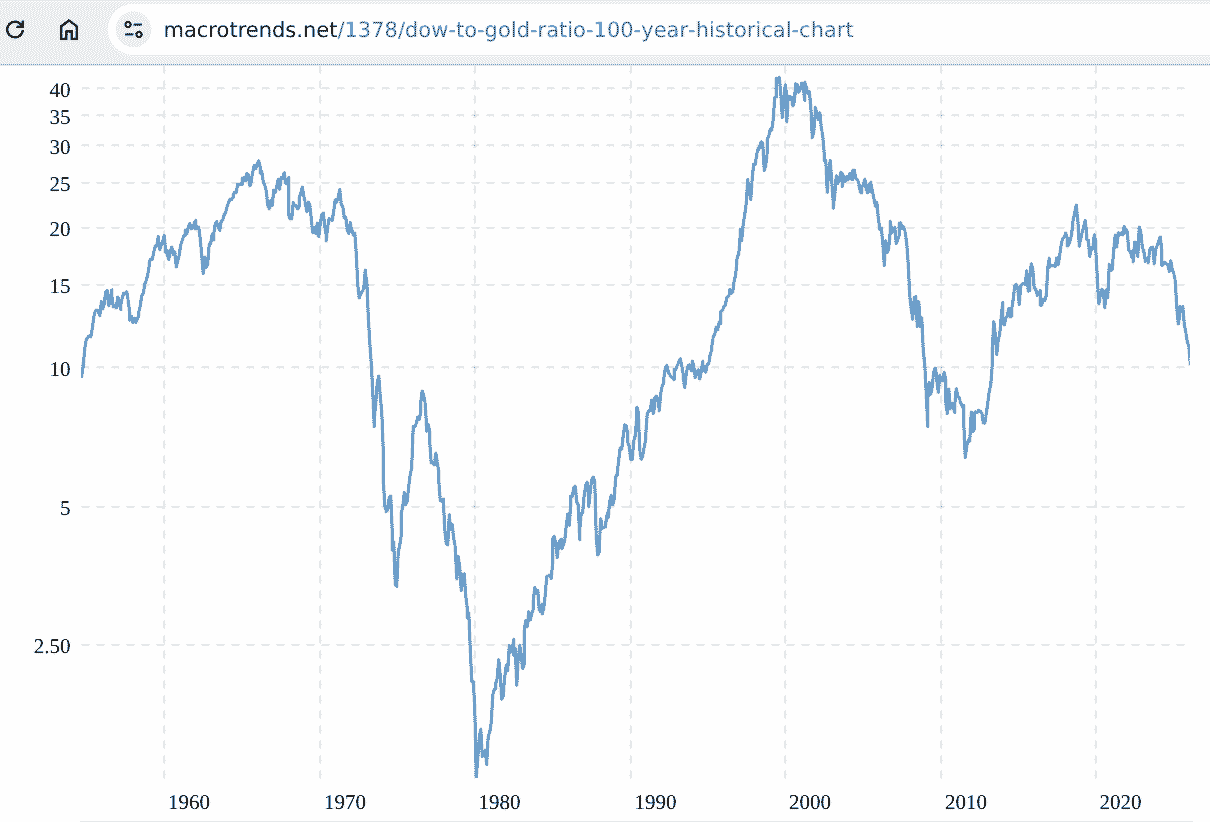

If you price in gold (as though it was money) rather than fiat dollars then historically the Dow price in ounces of gold ...

Do the same for T-Bills (accumulation) and CPI and both of those generally aligned with each other but in a generally downward slope manner, bought less gold (cost more dollars to buy gold) over time. Adding the dividends that the Dow provided to T-Bills made that downward slope more flat. Gold has more reflected M2 - debasement of dollars/debt expansion, which is increases faster than does CPI - that is slowed by productivity.

So generally gold, Dow (price only), T-Bills with the Dow dividends added might be considered as each broadly yielding flat lines (comparable to gold), but in varying volatility manner and where as the CPI downward slope line compared to just T-Bills alone that collective three way set > inflation. Yearly rebalancing and given historic wild extremes in volatility adds the potential to capture add-low/reduce-high 'trading' benefits. For instance in 1980 it cost a little more than a ounce of gold to buy a Dow stock index share, in 2000 it cost around 40 ounces (a single Dow share bought 40 ounces of gold).

The other main feature is that a combination of T-Bills perhaps with T Direct, physical gold in your possession and stocks held in a brokerage has more diverse counter party risk.

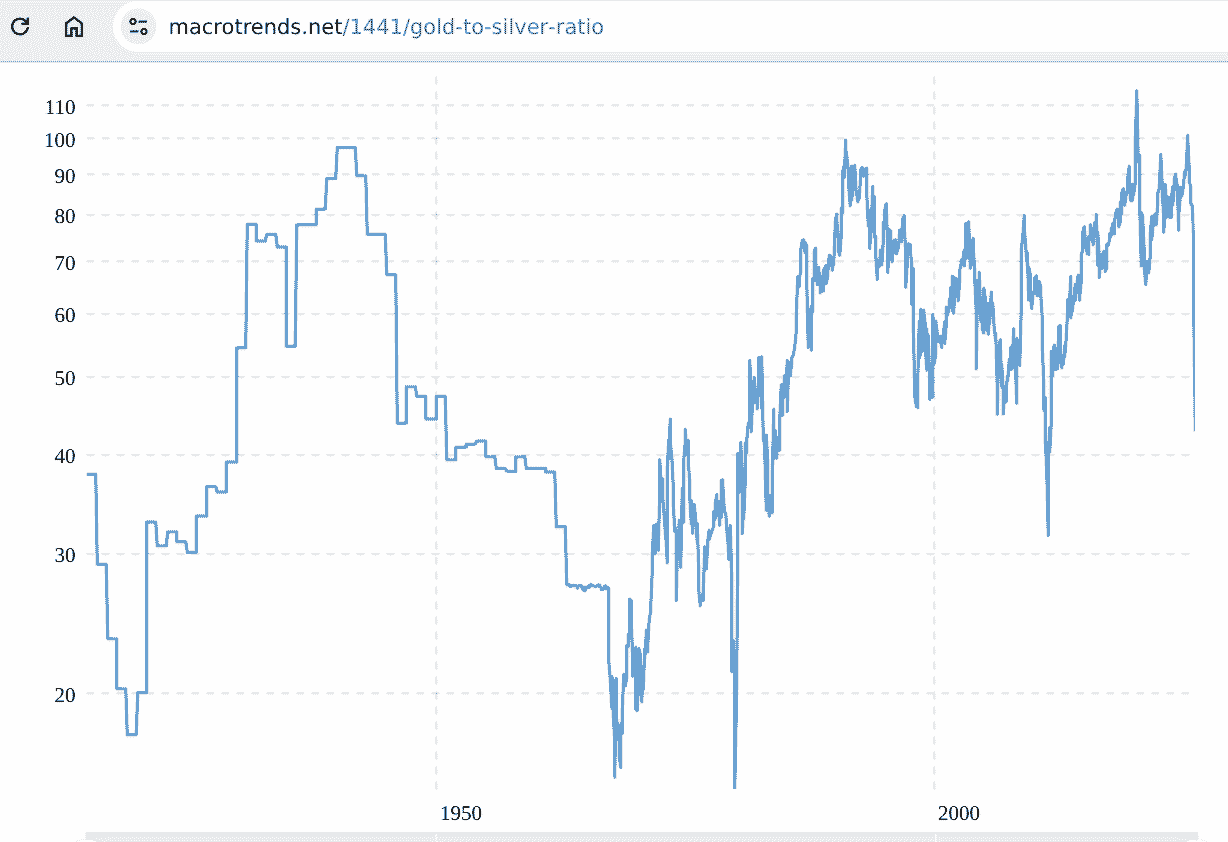

The relative stability of the baseline stock/gold/T-Bill asset allocation might be further worked to value-add (alpha), be more selective about 'bonds' (longer dated when yields are high/riskier or other alternatives/whatever); And/or perhaps swap out some gold for some silver when the gold/silver ratio is high and swap the silver back again to gold when the gold/silver ratio declines/is-low

Not long ago the gold/silver ratio was over 100, a ounce of gold bought 100 ounces of silver, more recently it has declined to around 50, the 100 ounces of silver you hold bought for a ounce of gold now buys two ounces of gold ... type 'trading'.

Yet another option is to transition to a more aggressive asset allocation as/when stock values are low (during/after deep dives), when the stock/gold/T-Bill asset allocation may have declined much less than stocks (buys perhaps twice as many stock shares than previously).

Optionality.